The real estate market faces challenges amid uncertainty surrounding interest rates. Despite this, industrial real estate is poised for robust performance in 2024, bolstered by sustained e-commerce growth.1

Meanwhile, multifamily sectors may witness rent growth due to high occupancy rates and a limited supply of new units. Property management is anticipated to experience growth, supporting the broader commercial industry. As investors continue to view real estate as a favorable investment, demand for property management services rises.

Property owners increasingly rely on managers, consultants, and asset managers to enhance profitability.2 Service consolidation aims to diversify revenue streams while technological advancements drive efficiency gains in property management. With mortgage rates remaining high, homeownership remains challenging, prompting stability in rental markets.

Market Outlook

Property

Predominant marketplace trends are not apparent.

Rate changes and terms have been inconsistent, which shows absolute increases as a normal course of business is waning.

New capital is entering the property space and there is a willingness to consider more CAT accounts.

Reinsurance continues to be a hurdle for markets to quote significant lines.

Buyers have experienced rate increases for four to five consecutive years, leading to rate increase fatigue.3

Carriers seek more data before risk placement to ensure optimized pricing. Building maintenance and upgrades remain a top data point for carriers. Sprinkler design especially for frame is critical.

Carriers and reinsurers continue to focus on proper valuation with upward valuations. The implications of the reinsurance marketplace are considering the geographic spread of risk.

The risk and increase of severe convective storms are at the forefront of every underwriter’s due diligence.

Excess & surplus lines (E&S) markets may offer more flexibility in the habitational space.4

Wildfire modeling is becoming a greater priority for carriers and underwriters as significant wildfire events are costly and more consistent.

Data and analytics are key to enhancing competitive quotes from most markets.

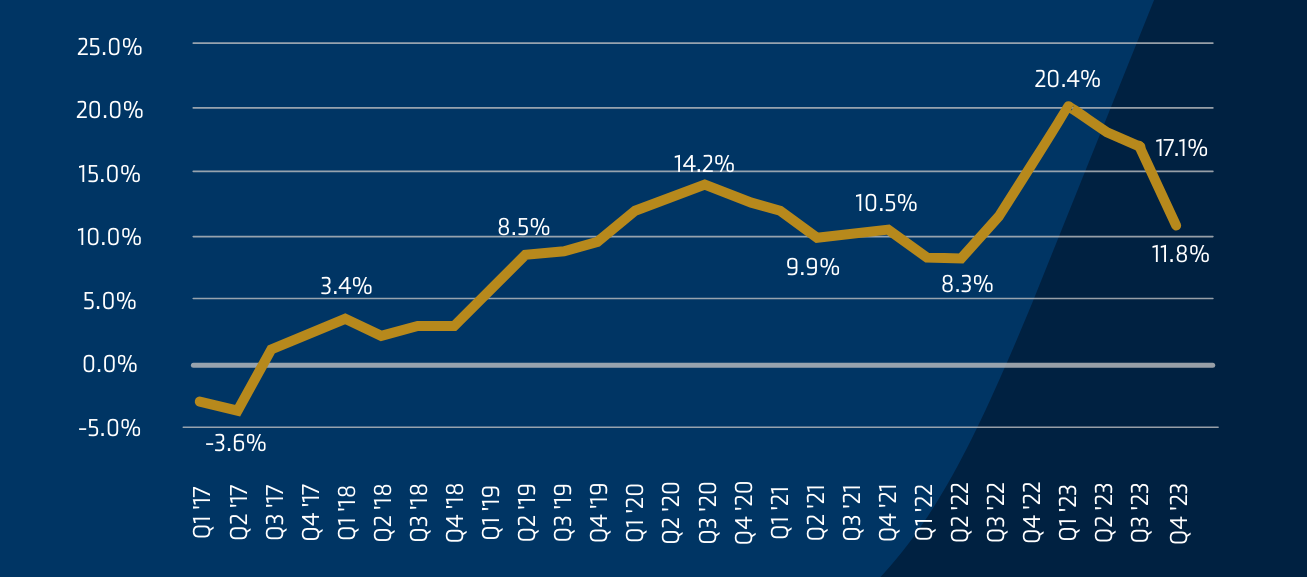

PREMIUM CHANGE FOR COMMERCIAL PROPERTY | Q1 2017-Q4 2023

Source: CIAB Commercial Property/Casualty Market Index Q4 2023

General Pricing Estimates

Non-CAT exposed property with a favorable loss history

Up 10% to 12%

CAT exposed property with favorable loss history

Up 15% to 17%

Casualty

General Liability

The multifamily sector is experiencing ongoing challenges due the sharp rise in Assault & Battery claims and ensuing litigation. Because of this, the E&S market is growing in this space every year. Venues such as Georgia and Louisianna remain some of the most challenging.

Admitted and E&S carriers have exited the market in Florida, Georgia, and Texas.5

Major cities that are seeing a rise in crime may see insurers compensate by implementing policy sublimit or excluding losses based on using crime scores in the underwriting process.

Excess Liability

Capacity is available at a higher premium.

General Pricing Estimates

General Liability

Up 15% to 20%

Umbrella & Excess Liability – Middle Market

Up 15% to 20%

Workers’ Compensation

California, New Jersey, and New York exhibit signs of hardening due to increased litigation claims costs and medical inflation. These states typically lead market shifts, prompting experts to monitor for potential ripple effects in 2024 and beyond.6

Auto

Auto carriers continue to be plagued by nuclear verdicts and rising medical costs.

Profitability has not been achieved in the last five years as an industry.

Finding carriers willing and able to offer coverage limits for hired and non-owned autos remains a change.5

General Pricing Estimates

Workers’ Compensation

Slight decrease to up 5%

Auto

Up 10% to 25% Up 20% to 30%+ if large fleet and/or poor loss history

Executive Risk

Cyber

The average cyber premium increase was under 1%.7 Most cyber programs have seen year-over-year rate decreases between 5-10% range over the last quarter.

Additional underwriting capacity has been steady in the market.

Social engineering and invoice manipulation schemes persist as common threats. Cyber markets are now assessing whether insureds require employees to verify any request to change payment instruction by calling back third parties on the phone, potentially leading to increase limits for social engineering losses.

Underwriters have started to focus on how insureds will monitor their IT security posture with third party technology.

Major Claims In the Sector

Wrongful Death

$140 Million Verdict: The decedent attempted to escape his apartment complex during a fire but tragically lost his life in the process. Subsequently, his family filed a lawsuit. Jurors awarded $140 million.8

Contact

Jim Litterer

EVP, National Real Estate Practice Director