The National Oceanic and Atmospheric Administration (NOAA) reports that 2024 experienced several severe climate anomalies, including snowstorms and tornadoes, which resulted in significant financial losses and made it the fifth warmest year on record.1

The property and casualty insurance landscape is evolving in response to these challenges. Private equity investing and financing plaintiffs’ bar on high profile litigated cases underscores a heightened focus on insurers taking cases to a jury verdict. Wildfire exposure and potential vacancies pose additional challenges. Despite these obstacles, building and renovation activities are rising, although high interest rates and regulatory complexities continue to pose difficulties.

In response to increased economic pressures, property owners are increasingly prioritizing ground-up construction on owned land. However, the higher cost of debt capital is limiting new construction initiatives. This economic climate has led potential developers to reassess projects amidst rising commercial vacancies and stricter financing conditions. Elevated interest rates are causing a slowdown in construction as developers face challenges such as slowing net operating income growth, increasing cap rates, and limited permanent financing.2

This cautious approach in the construction industry is further complicated by the ongoing housing shortage in major cities, which stands in stark contrast to the strong demand for affordable and workforce housing. B and C class properties experienced a 4.6% vacancy rate in 2023, compared to 6.5% with luxury properties.3 Property managers adapt their strategies to navigate easier building permit processes and mitigate economic risks.

Looking ahead, the commercial real estate outlook for the second half of 2024 remains cautiously optimistic. Despite lingering concerns, the multifamily, industrial, and retail sectors continue to perform well. Office vacancies are increasing in the high-interest rate environment, impacting overall sales volume.4 Major metropolitan markets like Los Angeles show strong multifamily performance.5 Chicago maintains stability6, and New York demonstrates resilience.7 However, the enduring impact of high interest rates remains a critical factor influencing market dynamics.

Market Outlook

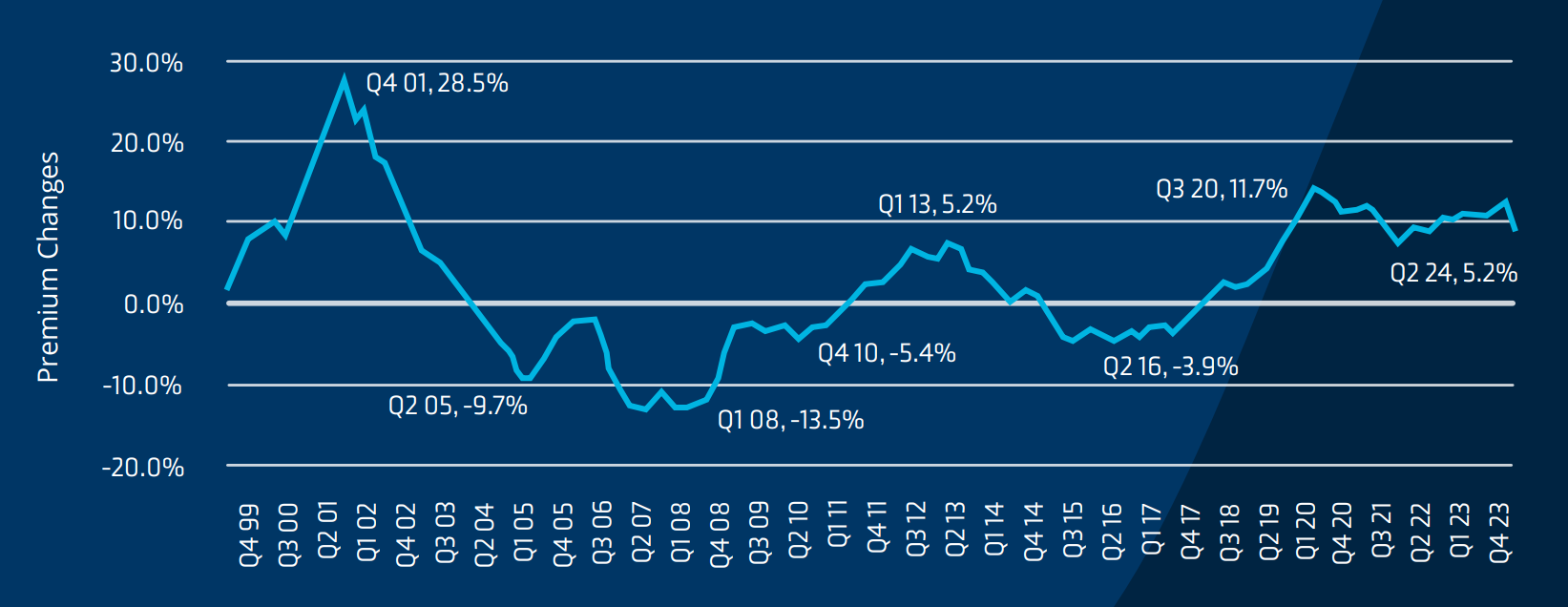

AVERAGE PREMIUM CHANGES Q4 1999-Q4 2024

Source: CIAB Commercial Property/ Casualty Market Index Q2 2024

GENERAL PRICING ESTIMATES

Non-CAT exposed property with a favorable loss history

Slight decrease to up 15%

CAT exposed property with favorable loss history

Up 10 to 40%

Property

Commercial property premium’s average increase was 8.9%, while the average premium increase across all commercial coverage lines was 5.6% in Q2 2024.8

Although the insurance market has reached a certain level of stability, specific sectors, classes, regions, and historically challenging accounts continue to face significant pressure. The market remains susceptible to disruption from external shocks or unforeseen events.

Property values are projected to increase by at least 4%, aligning with inflationary pressures on labor and materials.

Standard markets are narrowing their risk appetites and applying stricter underwriting discipline, particularly for portfolios with losses or CAT exposure. The risk appetite for frame construction is almost nonexistent.

The most shared and layered renewals are seeing reductions. London syndicates convey the presence of a soft market.

Admitted markets are shrinking, while the E&S market remains robust, open for business, and demonstrates a realistic pricing approach.

Premiums continue to surge into the E&S market, with a corresponding increase in policy count, indicating the likely presence of new entrants.

Reinsurance markets within the E&S space have remained stable. However, the property market is significantly impacted by secondary perils, including severe convective storms and inflation. According to Swiss Re, 50% of global secondary peril losses are attributed to severe convective storms, with hailstorms comprising many of these losses.

Casualty

General Liability

The general liability average premium rose by 5.1%.8 Nuclear verdicts continue to impact general liability.

Insurers are increasingly demanding detailed information on past losses and implementing preventive measures.

The commercial general liability market is expected to see rising premiums and stricter terms and conditions, driven by each organization’s risk profile and loss history.

Significant reserve uptakes from major insurance carriers were observed in Q4 2023.

2024 marks a re-hardening phase for general liability (GL) and excess (XS) insurance markets. Executives, underwriters, and brokers confirm that GL and XS rates are increasing from high single digits to low teens.

Excess Liability

Insurance carriers struggle with sufficient premiums to maintain profitability, exacerbated by nuclear jury verdicts and escalating claims frequency.

Social inflation, driven by millennial jury biases, anti-corporate sentiments, and the rise of litigation financing, continues to drive up costs and escalate verdicts.

In 2023, there were 89 verdicts exceeding $10 million, marking a 27% increase from the previous year. Twenty-seven claims exceeded $100 million—the highest number since 2009. The urgent need for broad-based tort reform is evident.

A few excess liability insurance providers have withdrawn from Georgia due to litigation concerns.

General Pricing Estimates

General Liability

Up 5% to 20%

Umbrella & Excess Liability – Middle Market

Up 5% to 10%

Workers’ Compensation

Workers’ compensation premiums constituted a diminishing portion of the P&C market, declining to 5% in 2023 from almost 8% in 2022.9

Net written premiums for private workers’ compensation rose by 1% to $43 billion in 2023, up from $42.5 billion in 2022.9

Premiums continue to hinge on risk factors and carrier availability.

Auto

Commercial auto premiums increased by an average of 9% in Q2 2024.8 Vehicle repair costs have risen, leading to higher claims costs and premiums.

Auto carriers face significant challenges due to nuclear verdicts and rising medical costs.

GENERAL PRICING ESTIMATES

Workers’ Compensation

Slight decrease to up 8%

Auto

Up 10% to 20% Up 25% to 30%+ if large fleet and/or poor loss history

Executive Risk

Cyber

In the first quarter of 2024, cyber insurance premiums were 12 percent more likely to change than in the previous quarter.

The size of premium reductions tapered off while the number of policies seeing decreases jumped by 8 percent.

Insurers maintain consistent underwriting standards, emphasizing fundamental cyber hygiene practices and the necessity of a cyber business continuity strategy.

Directors & Officers (D&O)

Overall market conditions have remained favorable in the first half of 2024. D&O pricing for recent renewals are generally more favorable, particularly for post- IPO and post de-SPAC companies.

Many D&O carriers and reinsurers have publicly stated that current rates are not sustainable.

The current pricing environment is influenced by the combination of new capacity entering the market and fewer IPOs and de-SPAC transactions.

However, the impact of increased litigation and IPO activity on pricing is yet to be determined.

Major Claims in the Sector

Personal Injury

$13.1 Million Verdict: The plaintiff sustained a quadriceps injury after slipping on a sidewalk outside an apartment building. This has resulted in mobility challenges, making walking difficult and necessitating an alternative approach to using stairs. Jury awarded $13.1 million.10

Contact

Jim Litterer

EVP, National Real Estate Practice Director