Retail space is expected to remain limited in 2025, as high cost of financing new or expanding projects is not justified by market rental rates. Yet, lower availability could lead to increasing rental prices especially in the more desirable locations such as strip malls and centers with grocery store anchors. E-commerce growth will continue to affect brick-and-mortar locations, as the online share of total retail sales are project to grow from 23% in 2024 to 30% by 2030.1 With this continuing shift in consumer buying habits, retailers are shrinking their footprints, particularly in malls, and focusing on smaller locations such as strip malls and open-air neighborhoods, in order to facilitate online purchase pickups and returns.

Office construction spending gained 1.8%, due in part to the Census Bureau classifying data centers as office space. In fact, data centers made up 3% of all commercial spending in 2024. Expectations for 2025 are optimistic yet cautious, data center construction is expected to continue positive growth2 but there is concern that growth will not keep up with demand.

Supply chain resiliency leading to increasing reshoring should continue to give the industrial real estate sector a boost, especially in areas along the U.S. border with Canada and Mexico and core industrial markets. Third-party logistics (3PL) companies should lead growth in occupancy as continued outsourcing by retailers and wholesalers should keep 3PL’s share of industrial leasing at or near 35%.3 Nearly 40% of space built since 2023 remains unoccupied, and though occupancy is expected to increase, especially in primary market areas, first-generation space should remain plentiful.

Much of the multifamily construction in the U.S. is near or past peak and new starts are expected to be 30% below pre-pandemic average by mid 2025, yet new supply is expected to be added in the Sun Belt and Mountain regions. Shrinking construction pipelines, strong renter demand, rising occupancies and accelerating rent growth are expected across all markets in 2025.4 Many of the areas past peak are realizing growth in terms of vacancy rates and average rent and that should continue throughout 2025.

Market Outlook

Property

Through September of 2024, catastrophe losses accounted for 8.8 points on the nine-month combined ratio, down from an estimated 10.0 points in 2023.5

The property and casualty (P&C) insurance and reinsurance pricing cycle has peaked in many areas and expect prices to flatten or with only minor declines.6

Innovation flood modeling at the property level is a tool that private insurers find offers real-time, property-level risk assessments that can bridge gaps between private and public data.7

Q3 saw continued price normalization driven by improved capacity and competitive pricing.8

2024 seasonally adjusted construction estimate rose in October to $2,174 billion, 0.4% higher than the September estimate. The overall 10-month 2024 construction spend is $1,814.8 billion, 7.2% higher than the same period for 2023.9

Property markets remain moderately impacted by natural catastrophes resulting in coverage limitations and structure changes.

Direct writers have a limited approach and are evaluating the reinsurance marketplace to make broad stroke changes to their business strategies.

Accounts with exposure to catastrophe events will continue to encounter challenges as insurers maintain their risk management. Despite the influx of new capacity into the market, fully comprehending the implications and market dynamics remains premature.10

Renewal outcomes will vary based on geography, occupancy, and loss records, resulting in a diverse and segmented market.

GENERAL PRICING ESTIMATES

Non-CAT exposed property with a favorable loss history

Down 10% to up 5%

CAT exposed property with a favorable loss history

Down 15% to 5%

Casualty

General Liability

Rate increases will continue as the legal environment remains volatile, resulting in larger premiums. Coverage remains available, but selective.

Coverage restrictions and underwriting scrutiny will continue due to increases in claims.

Excess Liability

Market remains stable with newer entrants in the market adjusting rates due to early claims.11

Primary layers are available with few carriers. The ability to build up with additional layers of limits are contingent on program availability.

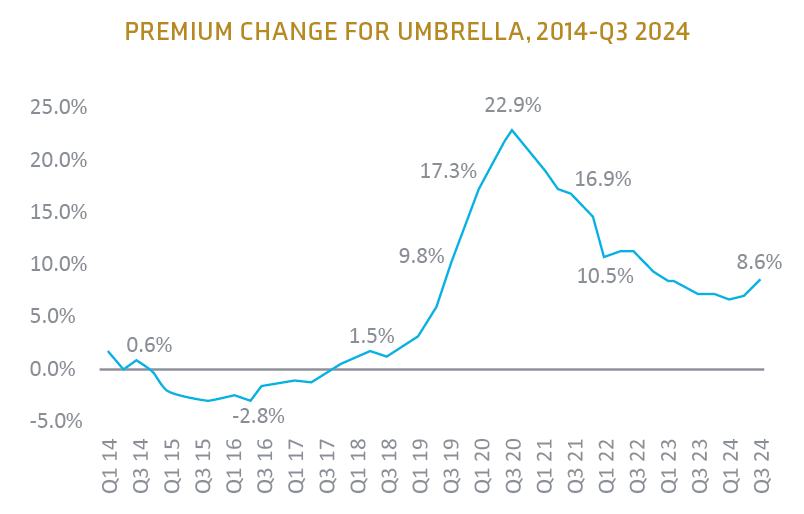

Premiums for the umbrella lines increased by 8.6%, largely due to carrier wariness and reduced capacity.12

Source: CIAB Commercial Property/ Casualty Market Index Q3 202413

General Pricing Estimates

General Liability

Up 10% to 20%

Umbrella & ExcessLiability

Up 15% to 25%

Workers’ Compensation

Workers’ compensation premiums continue to decrease, according to CIAB, falling 1.4% in Q3 2024.14

In the past year, lost time claim frequency decreased by 8%, continuing a long-term trend driven by improved workplace safety measures. These advancements, supported by evolving safety technologies, have contributed to consistent annual rate decreases across most U.S. states.

There remains a possibility of workers’ comp premiums increasing in 2025 due to wage inflation, reduced rates, and increased size of primary claims.15

For 2025, the National Council on Compensation Insurance has recommended a 6.1% overall average reduction in workers’ compensation premium rates for the voluntary market and 6.2% reduction in the assigned risk market.16

Auto

Commercial auto premiums rate increased 8.5% in Q3 2024, a slower increase than the previous quarter.17

Enhanced underwriting practices are anticipated to rapidly mitigate the substantial personal auto rate increases implemented over the past three years.

Fitch reports that successive substantial hikes in auto premium rates have significantly contributed to recent improvements in underwriting performance.

CPI data indicates that motor vehicle insurance costs increased by 50% over the three years from July 2021 to July 2024.18

GENERAL PRICING ESTIMATES

Workers’ Compensation

Down 1% to Flat

Auto

Up 8% to 19% + if large fleet and/or poor loss history

Executive Risk

Cyber

Cyber premiums decreased an average of 1.5% in Q3 2024, the second highest decrease among coverage lines.19

Frequency of claims increased 13% and claims severity was 10% from 2022 to 2023, and the average loss was $100,000.20

The most common attacks reported in 2023 were business email compromise (BEC) and funds transfer fraud (FTF). Together they made up 56% of all claims and FTF claims increased both in frequency and severity, with losses averaging over $278,000.21

Businesses of all sizes saw increases in claim frequency and severity. Businesses with less than $25 million in revenue experienced modest increases in both mid-sized companies, $25 million to $100 million, realized a 32% increase in frequence and a 9% increase in severity.22

Directors & Officers (D&O)

Although D&O litigation increased in 2024, overall market conditions remain favorable in the early part of 2025.

New capacity has entered the market during a period where IPOs and de-SPAC transactions have declined sharply. This combination of events has created more competition for legacy business.

Carriers do remain cautious regarding companies with near-term capital needs or a high likelihood of M&A.

It remains to be seen whether the increase in litigation and a continued uptick in IPO activity will have a material impact on the current pricing environment, although based on recent history it will take some time (and a noticeable increase in litigation) before pricing changes course.

The current market trends will continue with cautious optimism for the foreseeable future.

Major Claims in The Sector

$8.17 Million Verdict Plaintiffs were injured when a large tree fell on them while they attended a farmers’ market in 2019. One child and two adults were injured, with one of the adults suffering several spinal fractures. Jurors awarded a total of $8.17 million.23

$68.5 Million Verdict A Pennsylvania man died when he fell nearly 50 feet while working on a townhouse development in Pennsylvania in 2021. Jurors awarded $68.4 million.24

$38 Million Verdict Plaintiff was injured in a car accident and sued the North Carolina DOT claiming the crosswalk was poorly designed. Jurors awarded $38.24 million.25

Contact

Jim Litterer

EVP, National Real Estate Practice Director

Tyson & Mendes. (2024, June 28). $38M for NC Woman After Car Accident in Poorly Designed Crosswalk. Tyson & Mendes. https://www.tysonmendes.com/cases/↩︎