Executive Risk SolutionsQuarterly Update | April 2026

Apr 27, 2026

The Delaware Supreme Court recently upheld coverage for a settlement that resolved merger litigation, albeit on different grounds than the Superior Court. In affirming the lower court’s decision, but under a different rationale, the Supreme Court found the claims asserted by shareholders under Sections 14(a) and 20(a) of the Exchange Act did allege inadequate consideration; however, the insurers seeking to avoid their coverage obligations based on the “bump-up” exclusion failed to prove the settlement represented an increase in consideration.

“Much like the case in Towers Watson, allegations of inadequate consideration here were intrinsic to the theory of the Section 14(a) claim. Therefore, we disagree with the Superior Court’s conclusion that the first step of the Bump-up Provision was not met. However, the Bump-up Provision applies only if both steps are satisfied…[T]he second step will be satisfied only if Insurers can show that the ‘real result’ of the Settlement is that the Settlement Amount, or any portion of the Settlement Amount, increased the amount of deal consideration the shareholders received in the Transaction.”

The Court highlighted the fact that the settlement class was not limited to shareholders who received consideration in connection with the transaction and that the settlement was reached before either side sought to quantify the damages at issue. Since the settlement amount wasn’t arrived at or calculated based on inadequate deal price, it failed to meet the second requirement of the bump-up exclusion. Moreover, evidence was presented that the settlement amount was based on the cost of continuing to litigate the matter. With defense costs estimated to be in the range of $20-$25 million, there was ample evidence it represented something other than deal consideration. “[T]he Superior Court found that avoiding the cost of further litigation is a valid reason to settle and the Court has no reason to believe this reasoning was pretextual.” Illinois National Insurance Co., et. al. v. Harman International Industries, Inc. 2026 WL 204209 (Del . January 27, 2026).

The long-running coverage litigation between Under Armour, Inc. and its D&O insurers was heard by the Fourth Circuit Court of Appeals in late 2025. It involved the question of whether Under Armour was entitled to coverage under two separate D&O programs for the governmental investigations and securities class actions it faced. The SEC action was settled for $9 million, while the securities litigation was resolved for $434 million. The federal district court held in favor of Under Armour, reasoning that the enforcement action initiated by the SEC and the securities litigation were separate and unrelated for purposes of coverage. The Fourth Circuit disagreed, reversing the lower court and depriving Under Armour of $100 million in coverage available under the second D&O insurance tower.

D&O insurers initially accepted coverage for the securities litigation under the 2016-2017 program and the governmental investigations under the 2017- 2018 tower. The insurers subsequently amended their coverage position and sought to recoup all amounts advanced under the 2017-2018 program, taking the position the two claims were related and therefore constituted a single claim.

According to the appellate court, “The derivative litigation and the securities litigation involve claims about the public forecasts that Under Armour would continue to grow at the same pace despite the financial trouble, bankruptcy and liquidation of its major customer, Sports Authority. They also involve claims that, despite their optimistic public statements, Plank (UA’s CEO) and other officers used inside information to sell Under Armour stock at a substantial profit. The government investigations, at least when they began, involved these same issues. In its initial subpoena to Under Armour, the SEC requested, among other things, all documents concerning the company’s efforts to achieve a quarterly revenue growth rate of at least twenty percent.”

The appellate court went on to connect the enforcement action’s allegations of pulling revenue forward to make the company’s financial performance look better as being logically related to the conduct at issue in the securities and derivative litigation. “To get out in front of the negative financial impact that could follow from missing its 20% growth estimates due to poor market conditions, Under Armour pulled forward its orders, which allowed it to continue forecasting its 20% target publicly. Its actions, as part of a single scheme, stemmed from a single goal – to convince its shareholders and the public that it was achieving 20% growth in spite of the trouble with Sports Authority and the market generally. Thus, the pull forwards and the allegedly misleading public statements derive from the same cause – a desire to continue to hit its growth estimate.”

As we have detailed at length in prior Quarterly Updates, the issue of whether claims are related and therefore limited to coverage under one policy remains a very sensitive issue in the D&O market. Insurers are taking very unpopular positions and choosing to litigate the disputes, rather than work with their policyholders and find solutions. With such large sums at stake, this may be inevitable; however, it will be up to brokers and insurers to keep these disputes out of court. Navigators Insurance Co. et. al. v. Under Armour, Inc. 165 F.4th 171 (4th Cir ., January 20, 2026).

In another example of insurers seeking to have it both ways, the Delaware Superior Court ruled against insurers for their denial of coverage under a D&O insurance program. Here, an Insured provided notice of a Section 220 Books & Records demand made by a shareholder during its 2022-2023 policy period. The insurer denied coverage for costs associated with the 220 Demand but accepted it as a notice of circumstances which may give rise to a future claim. During the same policy period, an activist investor (Camac) filed a complaint in the Delaware Court of Chancery seeking additional books and records and then filed a preliminary proxy solicitation with the SEC, seeking support for two board nominees. Shortly after the policy period expired, the investor filed a lawsuit in 2023 alleging breach of fiduciary duty along with a derivative claim against the insured.

Given the timing of the lawsuit’s filing, notice was made under the subsequent D&O insurance policy as well as the prior policy, which were issued by different insurers. Both insurers sought to deny coverage, with the former taking the position the lawsuit was unrelated to the 220 Demand and the latter asserting it was related. The insured brought this case seeking a judicial declaration regarding which policy afforded coverage. Utilizing the ‘meaningful linkage’ standard, the Court found the 2023 lawsuit arose out of the same conduct at issue in the 220 Demand. “The circumstances described in the 2022 Demand were integral parts of Camac’s argument in the 2023 Lawsuit. Accordingly, there is a meaningfully [sic] link between the 2022 Demand which Wesco accepted as a notice of circumstances and the 2023 Lawsuit because they allege the same underlying conduct.”

We highlight this case as yet another example of the proverbial “finger-pointing” that can happen when claims span multiple policy periods with different insurers. It is deeply frustrating for an insured to receive denials from both carriers and be forced to litigate for coverage. Forte Biosciences, Inc. v. Wesco Insurance Co. et. al., 2026 WL 66768 (Del . Super ., January 8, 2026).

In another case out of the Superior Court of Delaware, one very likely to be appealed, the Court held that an investigation initiated by the Department of Justice amounted to an allegation of wrongdoing. In insurance parlance, the question before the Court was whether a Civil Investigative Demand (CID) constituted a “Claim” for purposes of coverage.

The facts underlying this coverage dispute involved the DOJ’s announcement in 2016 that it considered ‘one-way chart’ reviews performed by Medicare Advantage Organizations to be in violation of the False Claims Act. Thereafter, the DOJ issued a CID to Cigna, which in turn notified its insurers. Additional CIDs were issued to Cigna in 2017, 2018, 2020 and 2022. A Tolling Agreement was also executed in 2017 and extended several times. Notice was provided under Cigna’s 2016-2017 Managed Care Errors and Omissions policy that separately defined “Claim” and “Governmental Investigation”. While the publicly available opinion is partially redacted, it makes clear that Governmental Investigations are not afforded indemnity coverage.

The primary insurer, ACE (Chubb), initially denied coverage, but subsequently reversed its position and agreed the CID was a Claim. The two excess insurers disagreed and took the position the matter only qualified as a Governmental Investigation, which gave rise to this coverage action.

The primary policy defined a Claim as “any written notice received by [Cigna] that a person or entity intends to hold [Cigna] responsible for a Wrongful Act.” A Wrongful Act was defined as “any actually or alleged act, error or omission in the performance or failure to perform Managed Care Professional Services.” In holding the CID to be a Claim, the Court explained its reasoning as follows: “Delaware caselaw shows that a government CID seeking information to investigate specific alleged wrongdoing by recipient, demonstrates an intent to hold the receiver responsible for that conduct…[T]he CID requested information as part of a government investigation concerning actions by the recipient, Cigna, and suggested that conduct violated a specific statute… Accordingly, as in Conduent, the Court here concludes that the 2016 CID’s reference to an ‘investigation’ is not meaningfully different from an accusation that Cigna violated 31 U .S .C . § 3729 – that is a distinction without a difference.”

It will be interesting to see if the Delaware Supreme Court is asked to review this decision, as many liability insurance policies make a distinct difference in the coverage afforded for investigations versus other claims. The requirement of a wrongful act being alleged is typically what differentiates the two; however, this opinion blurs that line. The Cigna Group v. XL Specialty Insurance Co., 2025 WL 3884858 (Del . Super ., December 8, 2025).

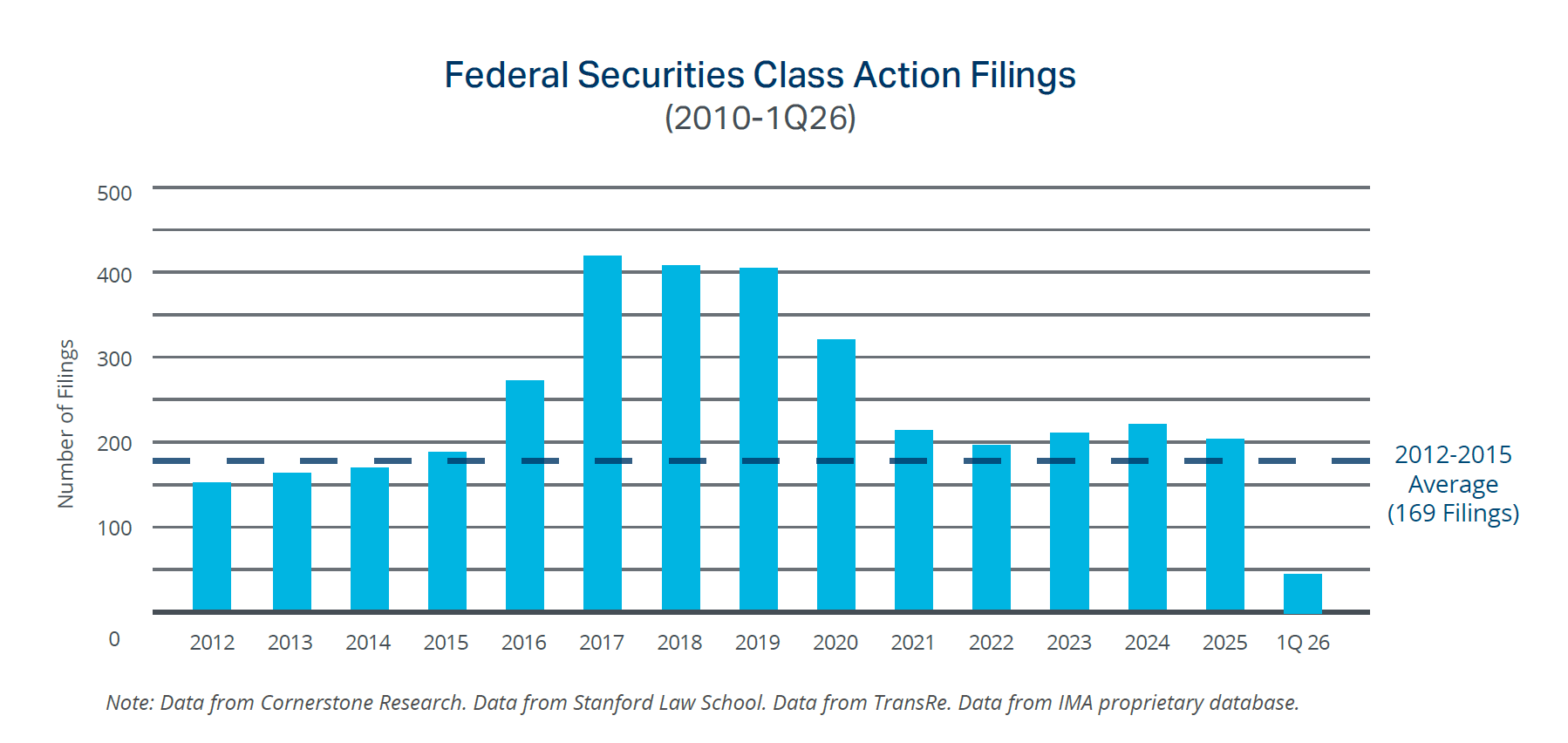

On February 6, 2026, a Complaint for Violation of Sections 10(b) and 20(a) of the Securities Exchange Act was filed against Masonite International Corporation. While we usually do not comment on newly filed cases, this one differs from your typical securities class action in the conduct being challenged.

On June 5, 2023, Owens Corning approached Masonite with a credible offer to acquire all the company’s outstanding stock for $120 per share, which at the time was trading at $94.09. The Masonite board of directors formed an Advisory Committee to analyze the proposal and engaged outside experts to assist in the process. During the time the offer was being evaluated, Masonite repurchased 79,000 shares of its own stock at an average price of $90.15. Masonite eventually rejected the first offer from Owens Corning but continued to engage with the company on a potential deal. Six offers were eventually made by Owens Corning up to a price of $133 per share. Masonite continued to repurchase shares of its stock throughout this timeframe. Following a failed attempt at an acquisition of its own, Masonite came to terms with Owens Corning and announced an agreement to be acquired on February 9, 2024. During the time it was in negotiations with Owens Corning, Masonite repurchased a total of 270,000 shares of its own stock.

The complaint filed against Masonite takes issue with the fact it never disclosed the offers it received from Owens Corning and continued to repurchase shares of its own stock at prices significantly below the offers presented. Claimants allege Masonite misled its shareholders, depriving them of the premium offered by Owens Corning. It goes on to allege statements made that the repurchases were done in compliance with Rule 10b5-18 were false because they were undertaken while in possession of material nonpublic information. Claimants assert Masonite, its CEO and CFO are liable for (i) making false statements; or (ii) failing to disclose nonpublic facts known to them and the true market value of its common stock. They further allege the share repurchases constituted a fraudulent scheme, as they (i) deceived the investing public regarding Masonite’s prospects; (ii) artificially deflated the market price of Masonite stock; and (iii) caused class members to sell Masonite shares at artificially deflated prices.

Claimants appear to be seeking the difference in share price between what was paid for the repurchased shares versus their true market value. Since this is a new angle of attack from the plaintiffs’ bar, we will monitor this case as it progresses. Central Illinois Carpenters Health & Welfare Trust Fund v. Masonite Corporation, et. al., Case 1:26-cv-01052 (S .D .N .Y).

Brian R. Bovasso

Executive Vice President &

Managing Director

IMA Executive Risk Solutions

303.615.7449

brian.bovasso@imacorp.com

Travis T. Murtha

Director of ERS Claims

IMA Executive Risk Solutions

Legal & Claims Practice

303.615.7587

travis.murtha@imacorp.com

Justin M. Leinwand

Product Leader

IMA Executive Risk Solutions

303.615.7773

justin.leinwand@imacorp.com

Daniel Posnick

Transactional Liability Leader

IMA Executive Risk Solutions

303.615.7747

daniel.posnick@imacorp.com

Emerging Liability Exposures in Advanced Manufacturing: AI and Robotics

Jul 6, 2026

Emerging Liability Exposures in Advanced Manufacturing: AI and Robotics

Jul 6, 2026

Emerging Liability Exposures in Advanced Manufacturing: Plastics Production

Jul 6, 2026

Emerging Liability Exposures in Advanced Manufacturing: Plastics Production

Jul 6, 2026

Hidden Risks Reshaping Energy M&A Outcomes

Jun 29, 2026

Hidden Risks Reshaping Energy M&A Outcomes

Jun 29, 2026

Hidden Costs of Deferred Maintenance in K-12 Schools

Jun 15, 2026

Hidden Costs of Deferred Maintenance in K-12 Schools

Jun 15, 2026