Education K-12 & Higher Education Market Update

Q2 2026

Educational institutions of all levels are navigating a challenging insurance environment. Both K-12 schools and higher education institutions are contending with hardening property and casualty markets, rising premiums, and increasingly complex risk profiles. Social inflation, high‐severity liability claims, aging infrastructure, and evolving threats—from cyberattacks to enrollment declines to greater SAM exposures—are reshaping how carriers underwrite and price coverage for the education sector.

K-12 schools are navigating a stabilizing property insurance market. The admitted insurance market has removed most risks with high-risk CAT exposures in prior years, causing schools to find coverage in shared and layered programs. Institutions may experience some rate relief in the shared and layered placements due to better than expected performance and greater capacity. The appetite for admitted markets remains firm for institutions with CAT exposed areas and those institutions in less prone CAT areas will see minimal increases compared to past years. Coverage typically addresses risks such as fire, natural disasters, and vandalism, but securing affordable, comprehensive coverage will remain challenging.

Premiums are rising and underwriting standards have tightened considerably. One of the more significant shifts affecting older school buildings is the movement away from “replacement cost” coverage toward “actual cash value” valuations— meaning that in the event of a loss, insurers pay only the depreciated value of a structure rather than the full cost to rebuild it. This change can leave institutions with meaningful coverage gaps, particularly for aging facilities.

Deductibles are also climbing, especially for specific perils. Wind, hail, and losses tied to older roof systems are increasingly subject to elevated deductibles, adding to the out-of-pocket exposure schools face after a claim.

On the coverage side, specialized endorsements are becoming standard considerations for K-12 programs. These include protection for computer equipment such as laptops and tablets, boiler and machinery breakdown coverage, and builder’s risk policies for schools undertaking expansion or renovation projects.

Deductibles are also climbing, especially for

specific perils.

Risk Management Trends

Insurers are placing greater weight on physical inspections and risk control surveys when evaluating school properties. The condition of buildings and maintenance practices can directly influence both eligibility and pricing. Once a specialized gap coverage, insurers now consider active assailant coverage as a critical component of a comprehensive school insurance program.

The casualty insurance market for K-12 institutions continues to harden, driven by rising costs and increased volatility, with institutions facing higher premiums, stricter underwriting standards, and concerns over social inflation and litigation, resulting in a surge of large, multimillion-dollar liability claims over the past few years.

While coverage remains available, insurers are increasingly cautious and expect schools to demonstrate robust risk management and prevention protocols. Carriers require extensive documentation, with many wanting five years of loss history and comprehensive exposure data.

While coverage remains available, insurers are increasingly cautious.

Cyber coverage for K–12 has been more challenging from a loss perspective. Claims from the PowerSchool cyber event continue to ripple underwriting for K‐12 institutions. While this event initially increased rates, it also drove tighter standards for core controls, which is now improving capacity and moderating prices.

Over the past decade, many states and the federal government have extended or eliminated civil statutes of limitations for SAM cases.1There is a clear trend toward restricting SAM coverage and tightening underwriting appetite, and many carriers have removed it from general liability policies. Incorporating risk management strategies and adhering to procedural and reporting obligations, institutions can demonstrate to carriers that they meet coverage requirements while also helping indemnify the institution against future suits and allegations.2

Risk Management Focus

Insurers want schools to invest in safety standards and protocols for staff, teachers, and volunteers. These should address situations like bullying, sexual misconduct, and campus security. Schools should also document practices for higher-risk activities, such as field trips and organized sports, to present at renewal as part of a school’s standard safety protocols.

The property market for higher education remains firm, yet stable, especially for institutions with strong data and minimal losses. Insurers are looking for detailed information on construction and maintenance, occupancy, and exposure. Incomplete data can affect rates and renewal options. The complexity of university and college campuses, which often include aging infrastructure, student housing, theft, and vandalism, presents a layered risk profile that carriers are pricing accordingly.

Underwriting guidelines have tightened in response to growing natural disaster exposures and the unique vulnerabilities of campus environments. Wind and hail coverage remain challenging.

Risk Management Strategies

Institutions that invest in proactive, well-documented risk management programs are better positioned to attract competitive terms and broader capacity from insurers. Mitigation strategies that can influence pricing and carrier appetite include conducting regular property inspections, maintaining complete records of maintenance and upkeep, and implementing disaster preparedness and recovery plans.

The property market for higher education remains firm, yet stable, especially for institutions with strong data and minimal losses.

The casualty market for higher education is firmly in a hard phase. General and excess liability lines are experiencing the sharpest rate increases, from high single digits to 15% and higher for institutions with poor loss records. Markets are implementing higher retentions and stricter terms, while prices are increasing due to the frequency of claims. Liability continues to contend with an increasingly challenged legal environment with exposures including sexual abuse and educators’ coverage, as well as the severity of nuclear claims.

Auto liability also remains under significant pressure. Workers’ compensation remains comparatively stable with significant capacity.

Higher education is experiencing a slight uptick in cyber premiums, but overall, this market remains soft, and capacity is keeping premiums flat or even slightly decreasing. Yet, carriers are focused on core controls, with particular emphasis on phishing awareness training for students and the presence of a formal incident response plan.

Underwriting scrutiny has also intensified around campus‐specific exposures, including student safety programs, campus police force operations, and overall security infrastructure.

Emerging Risk Areas

With the auto industry in a continuing hard market, auto and fleet programs should emphasize strong driver oversight and vehicle safety, including annual motor vehicle record checks on drivers transporting students, prohibiting student drivers, and ensuring routine vehicle inspections and maintenance.

As legal exposures increase for SAM, institutions should maintain a formal, written policy to prevent abuse, molestation, and misconduct that is supported by mandatory annual training for all personnel, with acknowledgment of compliance. Training may be conducted electronically or in person, and detailed records of completion may be maintained for every staff member.

Auto and fleet programs should emphasize strong driver oversight and vehicle safety.

No matter the institution, a loss of students equates to a loss of financial resources, which ripples through business and operational decisions. From a risk and insurance standpoint, the financial consequences are significant, impacting decisions by institutions regarding coverage and by carriers and underwriters who are looking more critically than ever at exposures.

For insurers, the enrollment cliff raises meaningful questions about the long-term financial viability of tuition‐dependent institutions, their ability to maintain facilities, and the sustainability of their risk management programs. Institutions that respond proactively— by diversifying their student pipelines, developing flexible program models, and right‐sizing their operations—will present a more stable risk profile than those that defer difficult decisions until financial distress forces their hand.

Under-enrolled buildings create operational inefficiencies and can accelerate deferred maintenance, increasing property risk exposure over time. In some cases, school closures become unavoidable, bringing their own wave of disruptions: staff reductions, student reassignments, and broader community instability. Institutions can approach enrollment loss strategically—using it as an impetus to redesign learning environments, build smaller and more personalized communities, and invest in wraparound student supports—and can build more operationally resilient institutions.3 For risk managers and insurers alike, institutions that treat this moment as a catalyst for thoughtful restructuring rather than a trigger for reactive cost-cutting can present a more stable and sustainable risk profile in the future.

Slip, trip, and fall (STF) incidents are among the most pervasive and underestimated risks facing educational institutions at every level. According to the National Safety Council, STFs accounted for 8.8 million non-fatal injuries and 47,000 deaths nationally in 2023.3 For schools and universities—with their high‐traffic hallways, aging walkways, athletic facilities, playgrounds, and seasonal outdoor hazards—the exposure is constant and year-round.

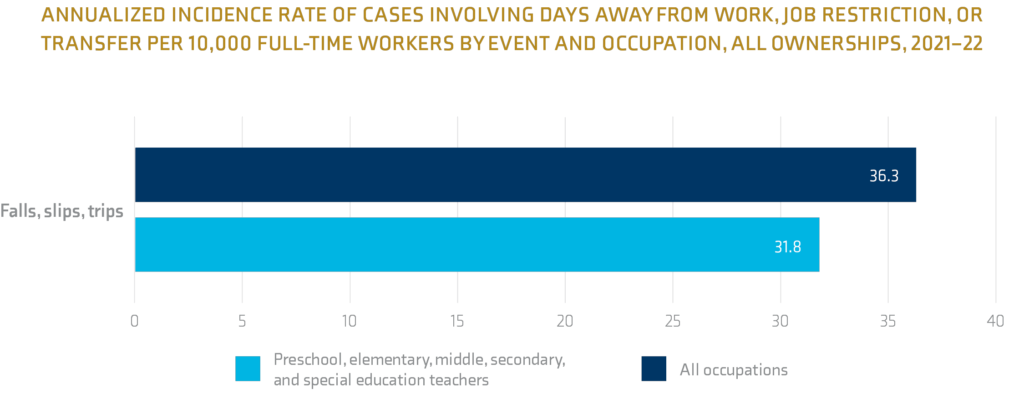

The consequences for institutions extend well beyond individual injuries. The average cost of a STF claim is $20,000, while the cost to legally defend such a claim can reach $50,000 or more.4 Negligence is a central factor: when a school fails to address a known hazard—an icy sidewalk, an unmarked wet floor, a cracked walkway—it faces significant liability for resulting injuries, including medical costs, lost wages, and pain and suffering. According to the U.S. Bureau of Labor Statistics, slips, trips, and falls represent 31.8 cases per 10,000 workers, almost in line with all other occupations at 36.3.5

Frequent claims erode an institution’s risk profile, driving up renewal premiums. And if a court judgment exceeds coverage limits, the school or district may be left responsible for the balance out of its own budget. Schools should also be aware that STF fraud is a real and growing concern—organized schemes have cost businesses and insurers tens of millions of dollars nationally.6

From an insurance standpoint, STF exposure touches multiple lines of coverage. General liability is the primary defense against third-party lawsuits from visitors and parents, covering legal fees and settlements. Student accident insurance fills gaps by reimbursing out‐of‐pocket medical costs for injured students, regardless of fault, reducing the likelihood that families will pursue litigation. Workers’ compensation addresses staff injuries. For public schools, sovereign immunity may offer some protection, but strict notice-of-claim deadlines—often as short as 60 to 90 days—mean that documentation and prompt response are critical from the moment an incident occurs.

Proactive prevention is both a safety imperative and a meaningful lever for managing insurance costs. Institutions should deploy entrance matting systems to capture tracked-in moisture, establish clear spill response protocols, and conduct regular audits of interior floors and exterior walkways for hazards as minor as a quarter-inch elevation change. Seasonal preparedness is equally important—formal snow and ice removal plans, temperature-sensitive signage, and well-maintained exterior lighting all reduce exposure during high-risk weather conditions. On the staffing side, requiring slip‐resistant footwear for custodial and food-service personnel and training staff to document and report hazards promptly demonstrates the kind of operational discipline that carriers look for. Institutions that can show improving safety metrics—including a declining Experience Modification Rate—are better positioned to negotiate more favorable premium terms at renewal.

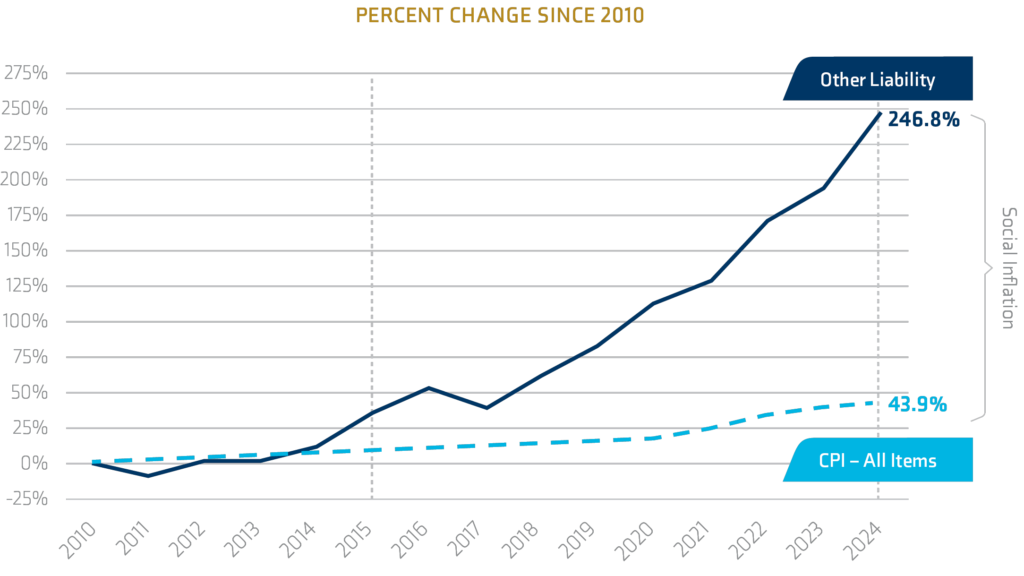

The ongoing rise in claim frequency and severity, driven by social inflation and nuclear verdicts, has pushed premiums higher, especially in liability lines. Due to their mission and operations, educational institutions at all levels face a range of exposures across property and liability lines.

The growth in reviver statutes at state and federal levels, whether statute of limitations is eliminated or extended, coupled with the largess of recent plaintiff awards in such cases, creates acute concerns for institutions. Detailed, thorough record keeping—including all communications—is a frontline defense that helps build strong resilience and, if necessary, a strong defense. A recent New York state court decision illustrates the importance of policy language and how small wording differences can have major financial implications.8

With exposures across property upkeep and construction, liabilities in employment, SAM, and auto, and limits—even gaps—in umbrella coverages, institutions must also be sure to navigate carrier and broker relationships. Broker expertise is vital in claims advocacy; expertise in handling claims across sectors— knowledge and experience that cannot be underestimated in identifying issues on site and in contracts, negotiating with multiple carriers, and providing timely and ongoing involvement until all matters in dispute are resolved.

The education insurance market—across both K-12 and higher education—is in a period of sustained hardening. Rising premiums, tighter underwriting, and an expanding range of liability exposures are creating real financial and operational pressures for institutions at every level. At the same time, schools and universities that invest in proactive risk management, maintain thorough documentation, and work with experienced advisors to tailor their coverage programs are finding meaningful opportunities to manage costs and protect their communities.

The path forward requires strategic planning, a clear understanding of evolving exposures, and a commitment to building the risk management infrastructure that carriers increasingly expect. Institutions that treat risk management as an ongoing practice—rather than a renewal-season exercise—will be best positioned to navigate the challenges ahead.

Derek Karr

National Education Practice Director

Debra Rosas

Vice President, Education Practice

Ryan Archer

Account Executive, Commercial Lines

Thomas Lipitz

Account Executive, Client Advantage

Angela Thompson

Marketing Strategist, Market Intelligence & Insights

Brian Spinner

Marketing Specialist, Market Intelligence & Insights