Private schools, colleges, and universities are increasingly facing a variety of discrimination-related requirements in areas including admissions, athletics, diversity, student care, and more. Being on the wrong side of these can be costly in terms of reputation and legal and professional liability.

Title IX civil rights mandates addressing discrimination are being applied in relatively new circumstances. Athletics is seeing the most recent development, which, under Title IX, ensures that men’s and women’s sports programs receive equivalent funding, equipment, exposure, facilities, scholarships, transportation, academic support, medical support, and more.1 The new Title IX regulations are under review to add protection for transgender student participation in athletics.2 The final ruling may be finalized in Summer 2024. If protections for LGBTQ+ are added to Title IX, it will be mandatory for institutions receiving federal funds to comply. Ramifications for noncompliance can result in fines, loss of federal funds, and various other issues.

The Department of Education’s Office for Civil Rights reminded schools covered under Title IX that they must offer a learning environment free from discrimination or harassment based on students’ national origin, ethnicity, or religion in response to the Israel-Hamas conflict. They also reminded these schools to keep their anti-discrimination policies current and ensure they abide by them.3

The recent U.S. Supreme Court decision significantly affected admissions by clarifying how a school can and cannot consider an applicant’s race. In short, race, as an element of a student’s personal story, can be a legitimate admissions factor, but considering a candidate’s race in and of itself cannot be part of the admissions selection process.4 Programs and student services provided by institutions with large minority groups can also face discrimination based on preference for those minorities or demand for additional services for those outside the minority groups. Best practices and services can be scrutinized, leaving intuitions open to lawsuits.

There are gray areas in some of these and similar mandates. Even the best-intentioned schools might find themselves justly or unjustly accused by someone who feels aggrieved in these areas and is looking for redress in the legal arena or the court of public opinion. Understanding the marketplace will be an important key to leveraging partnerships with broker and carrier partners.

Market Outlook

Property

Commercial property premiums increased by an average of 11.8% in Q4 2023.5

Increases to commercial property lines continue to be justified by catastrophe losses, reinsurance capacity, and pricing.

Accounts with exposure to catastrophe events will continue to encounter challenges as insurers maintain their risk management. Despite the influx of new capacity into the market, fully comprehending the implications and market dynamics remains premature.6

Renewal outcomes in the market will vary based on geography, occupancy, and loss record, resulting in a diverse and segmented market.

High-risk exposures may see more significant increases at renewal or conditional renewals.

Buildings that are well maintained and outside of wildfire zones are poised to have better renewal success.

Casualty

General Liability

Insurers request further details on previous losses and the steps to prevent similar losses.

The commercial general liability markets are expected to see rising premiums and more stringent terms and conditions based on each organization’s risk profile and loss history.

United Educators said the average cost doubled for their primary general liability and educators’ legal liability claims. Defense costs and larger award settlements are contributing to the increasing claims.13

Schools that violate Title IX may face legal consequences for discrimination, which may trigger the use of the school’s general liability and educators legal liability policy.

General liability coverage still sees losses related to slips, trips, and falls resulting in injury or damage.13

Sexual abuse and molestation within the general liability endorsement have experienced a surge in claims. Over the last 15 years, incidents of sexual misconduct have outpaced the growth of other claims categories.7

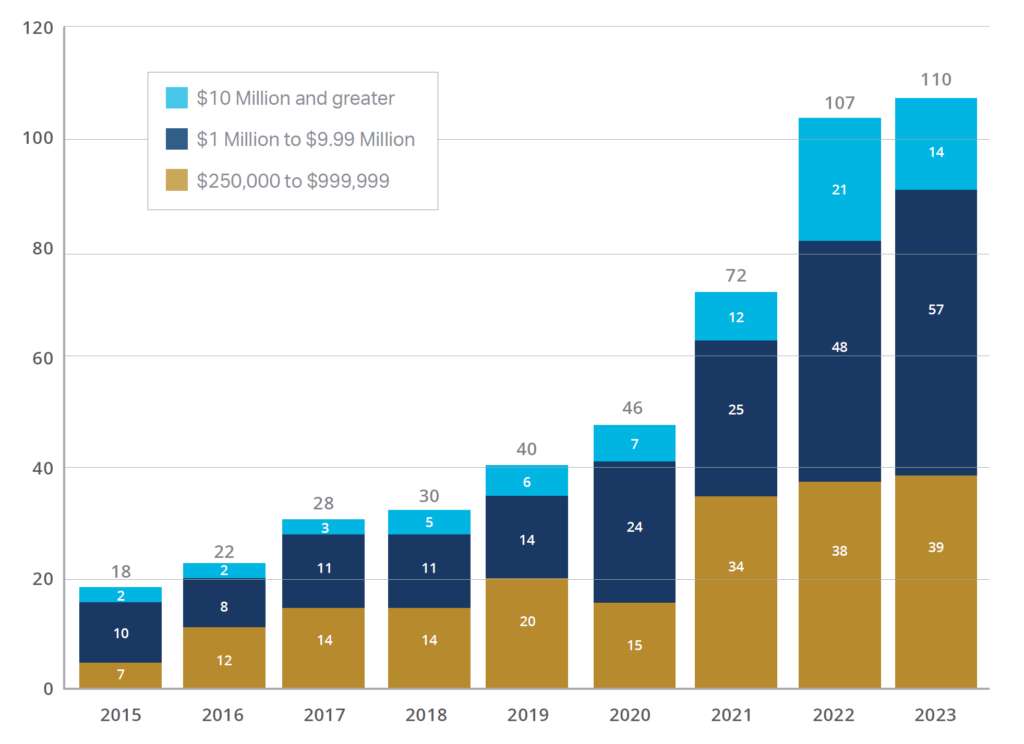

Damage Awards and Settlement Trends

Source: United Educators. An analysis of the Large Loss Reports from 2015-2023 shows troubling trends for K-12 schools and higher education institutions. Large Loss Report 2024. January 12, 2024.

Educators Legal Liability

The increase in individual education plans (IEPs) could lead to nonmonetary demands, prompting a need for additional services. Additionally, this scenario could potentially lead to lawsuits alleging discrimination in student services based on race, mainly if there is a preference for minority students.

Institutions that do not use race as a deciding factor are not prevented from being scrutinized as they relate to policies, best practices, and services.

Under the proposed changes, new reporting obligations will vary based on whether the conduct involves an employee or a student.

If the conduct constitutes sex discrimination against a student, the Title IX coordinator must be notified.

If the conduct constitutes sex discrimination against an employee, the employee must notify the Title IX Coordinator or provide the reporting party with contact information. Proper and prompt reporting will be instrumental.

Discrimination now ranks as the second most frequently reported settlement or award in public disclosures.13

Overall, capacity remains accessible for public officials’ liability, educators’ legal liability, and employment practices liability, with rates showing relatively stable trends.8

Excess Liability

Carriers are pushing for rate increases in 2024 to achieve better financial results and align with loss trends.

Creating a proactive narrative about an insured’s exposures, safety measures, and risk management culture and submitting a comprehensive and accurate application is crucial for securing sufficient capacity and impacting pricing outcomes.

Auto

Commercial auto insurance complexity persists, particularly with standalone non-owned auto coverage. Yet, bundling it with commercial package policies often opens doors to a more accessible market.

New regulations and rising repair and replacement cost for vehicles will drive the need for additional rate pressure from insurance carriers. Double digit rate increases for auto coverage will be common in 2024 renewals.

Workers’ Compensation

Enhanced mental well-being correlates with improved workplace safety and productivity. Prioritizing mental health initiatives can foster a supportive organizational culture.

The extended duration of workers’ compensation claims adds to the expanding financial risk, exacerbated by the increasing expenses linked to social inflation.9

California, New Jersey, and New York exhibit signs of hardening due to increased litigation claims costs and medical inflation. These states typically lead market shifts, prompting experts to monitor for potential ripple effects in 2024 and beyond.10

Cyber

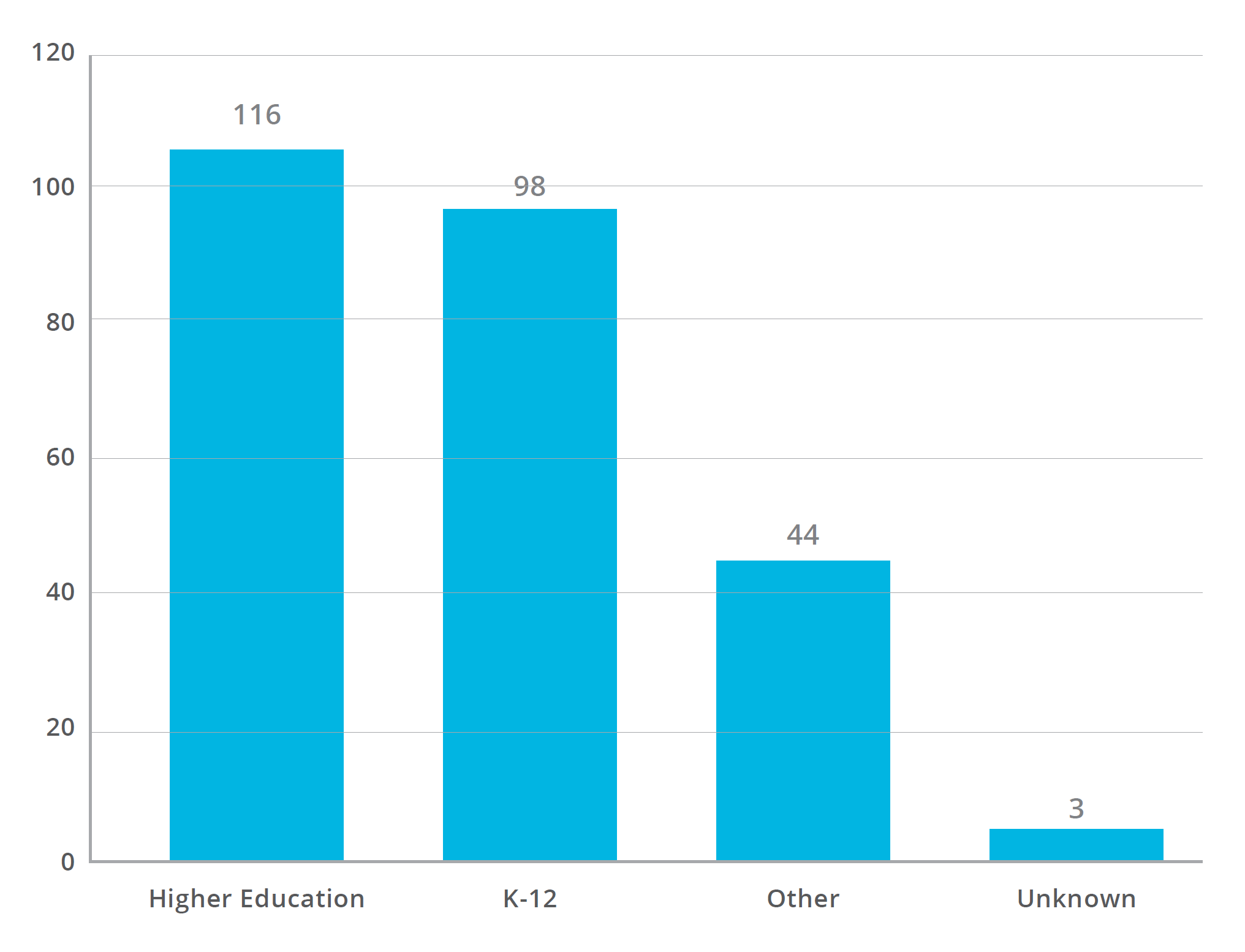

Ransomware attacks on K-12 increased 92% and 70% in Higher Education between 2022 and 2023.11

Recovery costs from a ransomware attack increased by less than 1% in K-12 and decreased by 25% between 2022 and 2023.12

The education industry’s most common entry points for threat actors are exploited vulnerabilities, compromised credentials, and malicious emails. YOY trends suggest that though the education sector is being hit with more ransomware attacks, schools are becoming more capable of mitigating loss by investing in cyber security and insurance.12

RANSOMWARE ATTACKS ON EDUCATION IN 2023

Source: ThreatDown Powered by Malwarebytes. K-12 vs Higher Ed Ransomware Attack on Education. 2024 State of Ransomware in Education: 92% spike in K-12 attacks. January 24, 2024.11

IMA’s Market Forecast for Educational Institutions

Insights from our top five carrier partners reveal anticipated rate expectations across various coverage lines. While our partners are committed to offering broad terms and conditions to educational institutions, premium increases are inevitable due to poor performance driven by social inflation, inflationary factors of labor and materials, the high cost of technology components, and perils such as wildfire and convective storms. Increased deductibles or reduced limits may be necessary for schools to share financial risk effectively and minimize overall premium increases.

2024 Budget Forecast for Insurance Premiums

Institutions with 5-year loss ratios under 40% (any paid amounts, expenses, and reserves divided by premium) should budget for 5-12% overall premium increases. Does not include exposure changes.

Institutions with 5-year loss ratios of 40% to 60% should budget for 10-25% overall premium increases. Does not include exposure changes.

Institutions with 5-year loss ratios above 60% should budget for overall premium increase above 20% with the possibilities of mandated changes in terms, deductibles, and retentions. Does not include exposure changes.

The Following Lines of Coverage will Generate the Largest Premium Increases

General liability, specifically sexual abuse, and molestations coverage; educators’ legal liability; and excess liability will be prone to higher rate increases than other lines of coverage in the insurance market. It remains difficult for insurance carriers to collect adequate premiums to keep these lines profitable due to nuclear jury verdicts and the continued increase in claims frequency.

Property – Insurance carriers will continue to apply pressure to insure property values to replace costs. Values will continue to be increased by 4% or higher to keep pace with inflationary factors of labor and materials. Still, there should be less frequency of double-digit value increases in 2024. This line of coverage will cause the greatest increase in overall premiums.

Changes in exposures, such as increased property values, enrollment changes, staffing/payroll changes, etc., are determined before the rate is applied. Any exposure changes can have substantial impacts on year-over-year premiums and should be considered in budget forecasts.

Major Claims In the Sector

Accidents & Crimes Resulting in Death

$19.5 million settlement: The Paramus school district in Paramus, N.J., settled for $19.5 million with two families affected by a bus crash. The crash, which occurred in 2018, resulted in the deaths of a teacher and a student. The family of the deceased 10-year-old received $12.5 million, while the family of a severely injured student received $7 million. The crash happened when the bus driver attempted an illegal U-turn on Route 80, causing a collision with a dump truck. The driver admitted to missing an exit and driving the bus across three lanes of traffic before the accident. In 2019, the driver pleaded guilty to several charges, including reckless vehicular homicide and was sentenced to 10 years in prison.11

Sexual Misconduct

$52 million settlement: The Sacramento City Unified School District and the city of Sacramento jointly settled for approximately $52 million after allegations of negligence regarding an after-school aide who was a sexual predator. The aide groomed and abused at least eight elementary school children, some as young as seven. Settlements in May 2023 included a $40 million payout to five victims, with the city covering about 60% and the district the remainder. A prior settlement with another victim also resulted in a $12.5 million payout. Joshua Vasquez, the aide, pleaded guilty in 2016 and received a sentence of 150 years to life in prison.13