In the first quarter of 2025, significant developments have affected educational institutions at every level, both public and private. While pressure from the federal government is now driving many institutions’ decision-making, many directives conflict with state guidelines that could create difficult decisions regarding the best way for institutions to proceed regarding policies, curriculum, funding, and parental rights.

Since January, several presidential executive orders have been issued that directly and indirectly affect educational institutions. The most impactful ones rely on enforcement of the administration’s interpretation of Title VI and Title IX. A brief overview of some of the executive orders with significant implications for education is included below.

Understanding the Recent Executive Orders

Each executive order impacting institutions, particularly as penalties for what is deemed non-compliance, has resulted in the threat of or direct loss of federal funding. For example, Columbia University faces the loss of $400 million in federal grants and contracts. A statement in March by Education Secretary Linda McMahon implied Columbia had not complied with federal antidiscrimination laws, “… universities must comply with all federal antidiscrimination laws if they are going to receive federal funding.”1 Columbia University has announced updated changes that align more with the administration’s policy interpretations. Yet, up to 65 colleges and universities are being investigated for reported infractions of the administration’s policies.

Administration cuts to other departments have also affected institutions that receive federal aid from different departments and programs. Johns Hopkins University cut over 2,200 jobs and faces an $800 million funding shortfall due to the unilateral cuts in the U.S. Agency for International Development (USAID). The job cuts included 1,975 international positions across 44 countries as well as 247 in the U.S, while another 29 international and 78 domestic employees will be furloughed with a reduced schedule.2

Improving Education Outcomes by Empowering Parents, States, and Communities calls for the closing of the federal Department of Education (DOE) and directs the cabinet secretary to facilitate moving DOE programs and agencies to other federal departments or back to state agencies. Federal funding makes up roughly 14% of most public school budgets, though it is over 20% for some states.3 The $1.6 trillion federal student loan portfolio will now be administered through the Small Business Administration.4 The EO also directs the DOE to “ensure that the allocation of any Federal Department of Education funds is subject to rigorous compliance with federal law and administration policy”.5

Ending Radial Indoctrination in K-12 Schooling directs federal, state, and local districts’ compliance with applicable federal laws regarding discrimination, curriculum, and parental rights included in Title VI, Title IX, FERPA, and PPRA and prescribes eliminating federal funding for non-compliance.

Ending Illegal Discrimination and Restoring Merit-Based Opportunity ends race- and sex-based preferences under Diversity, Equity, Inclusion (DEI), and Diversity, Equity, Inclusion, and Accessibility (DEIA) policies within federal agencies, and allows private sector enforcement under the 1964 Civil Rights Act, including institutions of higher education.

Expanding Educational Freedoms and Opportunity for Families expands K-12 educational choice and parental rights to choose which schools their children attend. The Education secretary will provide guidance on the use of federal monies for school choice. In contrast, labor, health and human services, defense, and interior cabinet secretaries will provide guidance on expanding educational choice for low-income families, military families, and students eligible for Bureau of Indian Education schools.

Additional Measures to Combat Anti-Semitism mandates federal agencies to report on education institutions’ efforts – particularly addressing higher educational institutions – in addressing anti- Semitic harassment and violence on par with discrimination against race and gender as dictated in Title VI of the Civil Rights Act of 1964.

Defending Woman from Gender Ideology Extremism and Restoring Biological Truth to the Federal Government focuses on sexual identity, stating that persons are born either of male or female identity, are only biologically of that gender, and cannot self-identify their sex and be granted protections under the 1964 Civil Rights Act. This executive order is at the heart of the dispute between the federal DOE and the government of Maine, specifically its Department of Education,6 with the federal government threatening to withhold education funds for what it describes as the state’s non-compliance.

Market Outlook

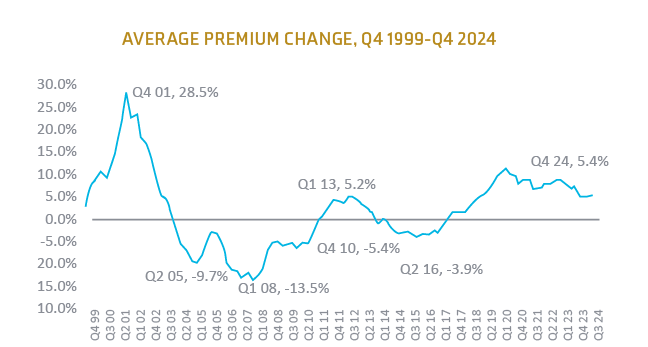

Source: CIAB Commercial Property/ Casualty Market Index Q4 20247

Property

In Q4 2024, the property insurance market stabilized significantly thanks to increased insurer and reinsurer profitability and new capital entering the market.

According to CRC Group, about 90% of client saw only single-digit rate increases, with 55% receiving no increase at all.8

Capital providers are optimistic, pursuing growth and driving competition.9

The London market is also showing stable market appetite for writing new opportunities in 2025.10

Premium increases driven by the Los Angeles wildfires are expected to take several months to emerge. When they do, the market may face greater challenges, especially as reinsurance renewals rebound from prior years. While the impacts will likely be concentrated in specific regions, the overall effects will be distributed across the industry.11 This and other recent catastrophic events will prompt (re)insurers to reassess tolerances for high-risk regions.12

Casualty

General Liability

Third-party litigation funding is an increasing issue, influencing claim values and litigation patterns.13

Liability continues to contend with an increasingly challenged legal environment with evolving exposures such as reviver statutes for abuse claims.

Capacity is available and stabilizing. Markets are implementing higher retentions and stricter terms, while prices are increasing for frequency of claims.14

Severity, or nuclear verdict trends, continues to rise, further feeding the need for rate increases.15

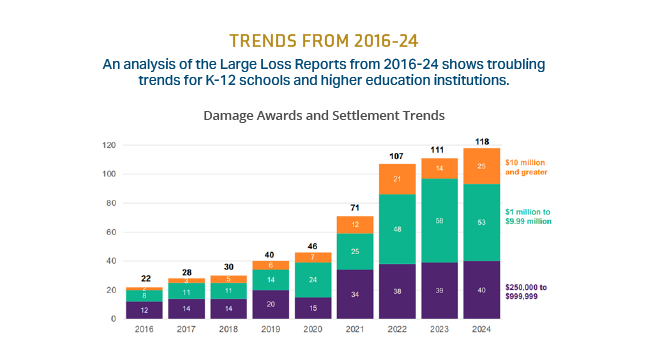

Source: United Educators. An analysis of the Large Loss Reports from 2016-24 shows troubling trends for K-12 schools and higher education institutions. Large Loss Report 2025, January 2025.16

Excess Liability

EPL is expected to increase by 10% except in California, where it is expected to increase by 20-25%.

Follow-form restrictions are becoming more widespread, including assault & battery, sexual abuse, and human trafficking limitations on coverage.

Verdicts over $10 million on average continue to push higher towards the $25 million mark.

The E&S market continues to have notable growth driven by a confluence of factors, including an increasing number of carriers in the market as well as flexibility and capacity.

Cyber crime is a growing concern in education, as well as mitigating data risks with cybersecurity practices.17 There are competitive terms for institutions that have implemented robust controls.

Auto

Rates are expected to continue increasing in the following year but there are signs of moderation.

By Q3 2024, growth of premiums in personal auto decelerated, growing by 11% year-on-year, down from 15% in Q2 24.18

Steepest rate hikes in 2025 could come from commercial auto with a 10% to 15% increase according to some experts.19

In the education sector, for monoline auto coverage, carriers generally don’t prefer non-owned exposure (volunteer drivers), making it difficult to place coverage. Many of the carriers that do provide this coverage have tight guidelines.

Commercial auto remains unprofitable, with the direct incurred loss ratio through Q3 2024 being the second highest in 15 years.20

Commercial auto had the highest average increases in premiums out of all lines in Q4 2024, at an average of 8.9%.21

The Council of Insurance Agents & Brokers (CIAB) reports that driver shortages, repair costs, and supply chain issues contributed to a surge in auto claim frequency and severity in 2024, citing that the average loss per commercial liability claim has doubled since 2014, leading to higher premium costs.22

Persistent social inflation pressure has also contributed to higher costs of claims.

Tighter underwriting controls expected in commercial auto.

Workers’ Compensation

Workers’ compensation experienced an average loss cost decrease of over 9% in 2024. Estimates expect a more modest reduction of 2% in 2025.23

Workers’ compensation premiums may rise in 2025 due to the combined effects of wage inflation, historically low rates, and the growing size of primary claims compared to premiums. This soft line of insurance may be coming to an end soon.

Market Forecast

As institutions navigate changes in federal policies and guidelines, understanding anticipated insurance premium changes is essential for effective financial planning. This forecast provides guidance on budgeting for insurance premiums based on five-year loss ratios, with specific attention to lines of coverage expected to experience the most significant rate increases. Key considerations include rising property values, increased claims in general liability, and adjustments in exposures such as property, enrollment, and payroll. Proactively incorporating these insights into your budget will help manage financial expectations and minimize unexpected losses.

Insurance Rate Outlook for Educational Institutions in 2025

2025 is expected to present significant challenges for insurance carriers offering risk transfer solutions to educational institutions nationwide. Factors such as nuclear verdicts driven by social inflation, political uncertainty, third-party litigation financing, antitrust lawsuits, expanded CAT exposures, favorable plaintiff jurisdictions, poor carrier performance on sexual abuse, employment practice, discrimination claims, and property issues are contributing to the need for higher rates on exposures.

In response to these challenges, education insurance carriers are adopting various strategies to address their concerns and improve performance. These strategies include reducing excess limits, tightening underwriting policies and procedures, increasing retentions and deductibles, and, unfortunately, increasing rates to remain viable options.

Anticipated Rate Adjustments:

General liability (GL): 8%-25%

Educators legal liability (ELL): 8%-30%

Excess liability: 8%-20%

Property: 4%-30%

Automobile: 8%-15%

Workers’ compensation (WC): -5% to 5%

California is expected to experience higher rate increases than the rest of the country. The percentage of rate increases will be significantly influenced by individual account performance, geographical location, and the size of the property schedule. Institutions with total insured values (TIVs) of less than $300 million will continue to face limited appetite from standard carriers and higher property rates. In comparison, larger TIVs of over $500 million will see a lower rate of need due to previous adjustments and increased carrier appetite.

Major Claims in The Sector

Accidents and Crimes

$129 Million Jury Award A jury awarded a Slidell, LA family $129 million after it found Our Lady of Lourdes Catholic School negligent in death of a six-year-old girl who was killed when struck by a car while she participated in an after-school running activity in the school’s parking lot.24

Sexual Abuse

$35 Million Settlement Bay Shore School District in Bay Shore, NY, approved a $35 million settlement brought by 12 former elementary school students alleging the district failed to protect them from abuse decades ago. The claims were made under New York’s Child Victims Act, which allows survivors of childhood sexual abuse to seek justice even if the abuse occurred many years ago.25

Discrimination

$4.5 Million Settlement The University of Colorado at Boulder will pay a total of $4.5 million in back pay to 386 female faculty members to settle a lawsuit contending the university conducted an equity review in 2021 that identified female faculty members were being paid less than similarly situated male faculty members. The university at the time failed to pay backpay as required under federal and state law.26

Guidance

Begin the renewal process early.

Partner with your broker early to prepare for any changes to increase greater renewal success.

Refine your statement of values.

It is important to review, update, and confirm your statement of values (SOV). Ensure your SOV reflects accurate property details and updates. This is crucial as property insurance constitutes a significant portion of your premium. Carriers are keen on accurate valuations, with construction costs rising due to inflation.

Partner with industry experts.

It is crucial to work with your broker’s industry experts, who understand the nuances of risk for educational-based institutions and the market when placing the specific risk. Collaborating with a team that can best represent your institution and partner with you is more critical than ever in this disciplined market.

We have a team solely dedicated to helping your institution manage cyber risks. We offer expert assistance, including coverage analysis, financial loss exposure benchmarking, contract language review, in-depth cyber threat analysis, and strategic development of comprehensive, high-value cyber insurance programs.

Engage loss control & claims teams.

Engage loss control teams before a claim begins by establishing robust loss control and risk mitigation with the help of your broker. We collaborate with you to understand your financial goals and operational challenges so we can help you identify, develop, and deliver risk control solutions that strategically mesh with your objectives and round out your risk management strategies to complement your insurance program.

Vasile, N. and West, Z. (2025, February 19). Cyber Premium Relief Continued While Auto Struggled for 54th Quarter, The Council’s P/C Market Survey Shows. Commercial Property/Casualty Market Index Q4 2024. Council of Insurance Agents and Brokers. https://www.ciab.com/resources/q4-2024-p-c-market-survey/↩︎