multifamily

Q2 2026 Multifamily

Market Trends

Insurance intelligence to help Multifamily owners achieve below market outcomes.

Q2 2026 Multifamily Insurance Considerations

Property Insurance Rate Decrease | 0-50%

Property insurance pricing is softening greatly in regions exposed to extreme weather events. Overextended carrier budgets and increased competition have created excess capacity, and much lower premium rates. We believe this will come to an end in the later part 2026 because inflationary pressures will begin to creep back into the insurance market. This will also impact the reinsurance market for 2027 which will also spill into the insurance marketplace putting even more upward pressure on pricing.

Liability Insurance Rate Increase | 2-8%

Although the insurance market for General Liability and Umbrella Insurance continues to be difficult due to a plaintiff-friendly legal environment, there is more capacity being deployed into the marketplace, allowing for additional options for clients to consider. These additional options only come to the surface by the broker pushing for them. Underwriters toggle rates by legal jurisdiction, down to the county level. Fortunately, liability premiums account for a minority of overall premiums, as such, multifamily owners are generally seeing per unit rate decreases. Property risk management procedures will influence getting the best outcome.

Limited Hurricane Activity (claims)

While the season had several powerful storms, many veered away from the US coastline, and no hurricanes made landfall on the mainland. This trend will reverse at some point creating upward pressure on pricing.

“Negligent Security” – Assault & Battery Exclusions

IMA is seeing a surge in gun, weapon & assault related “negligent security” liability claims — even when reasonable security measures, such as cameras and gated access are in place. As a result, obtaining adequate Assault & Battery coverage for this exposure has become increasingly difficult and costly. Many lenders now focus on this particular coverage as part of loan insurance requirements.

Thinking About Renters Insurance Differently

Requiring tenants to carry liability insurance can help protect your insurer’s balance sheet and lower your property insurance rates. While a minimum of $100,000 is common, we advise clients to require $300,000 in coverage. The higher coverage amount can have a meaningful impact on the rates carriers are willing to offer owners. Note: the cost to increase the limit is $3-6 per month per tenant.

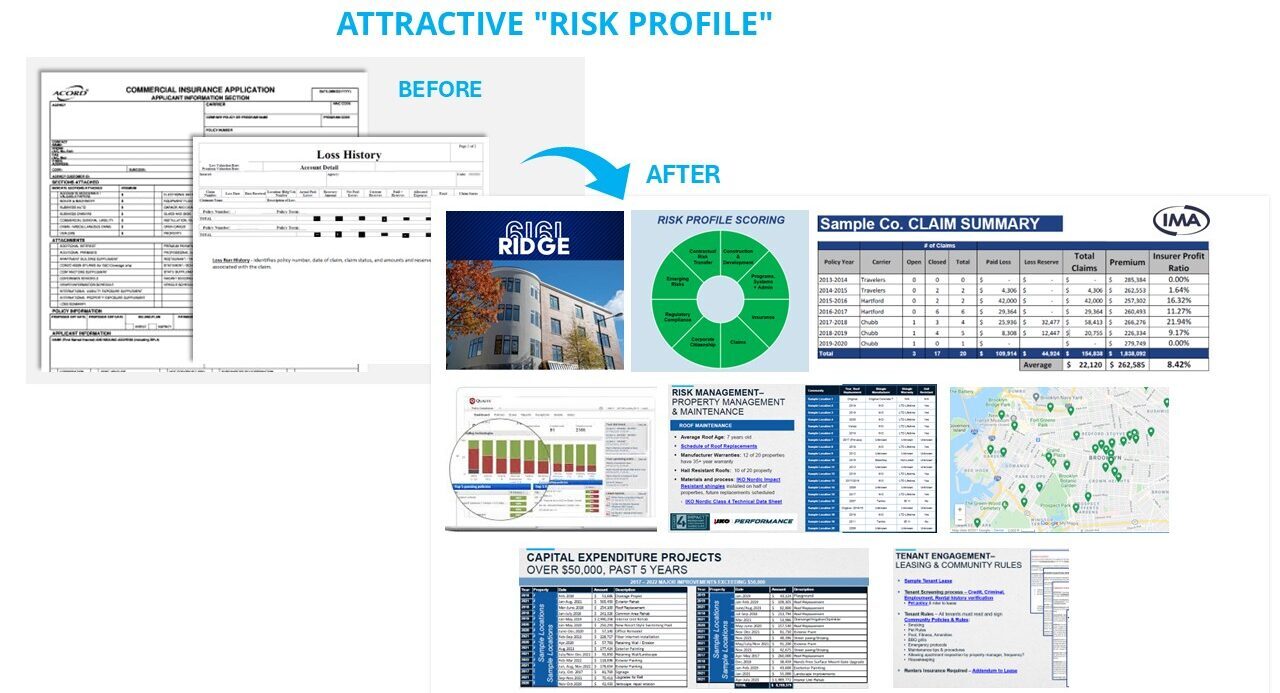

“Risk Profile” – Are your properties compelling to underwriters?

Conveying Property Management and Tenant Screening best practices is key to securing favorable terms from insurance carriers. Our “Risk Profile” presentation to the insurance market helps tell a highly compelling story to underwriters, achieving better insurance quote outcomes.

Underwriting New Deals – Don’t rely on standard “Per Unit” pricing (or the OM!)

Every asset deserves the eye of an insurance broker experienced with multifamily in each geography. Many factors go into insurance cost per unit. Allow IMA to give you an experienced cost per unit range based on current market conditions and recent deals on similar assets.

US Debt Affects Insurance Markets

The connection between Interest rates, Inflation, and over indebted Sovereign nations will play a big role with insurance pricing moving forward. The U.S. refinancing of their outstanding debt and the investment needed to reshore manufacturing and upgrade the electrical grid means more long-term Treasuries need to be sold. This alone is inflationary. Adding the labor and material needs to rebuild Americas manufacturing base and electrical grid upgrade will create immense upward pressure on pricing. To stabilize the government bond markets, the Treasury will print more money and may have to implement some form of yield curve control. Now more than ever insurance brokers need to understand the connection insurance has to global economics and the effects it has on premiums.

Surge in LIHTC Developments

As the construction cost and interest rate environment present new-build challenges, developers are turning towards LIHTC based projects. From an insurance perspective, it is critical to showcase the quality of construction and tenant screening practices in place to obtain the best outcome in the marketplace.

How are your assets/operations being presented to insurance carriers?

Contacts

Marbury SVP, Commercial Lines

Reyman SVP, Commercial Lines

Mandel Client Manager, Commercial Lines