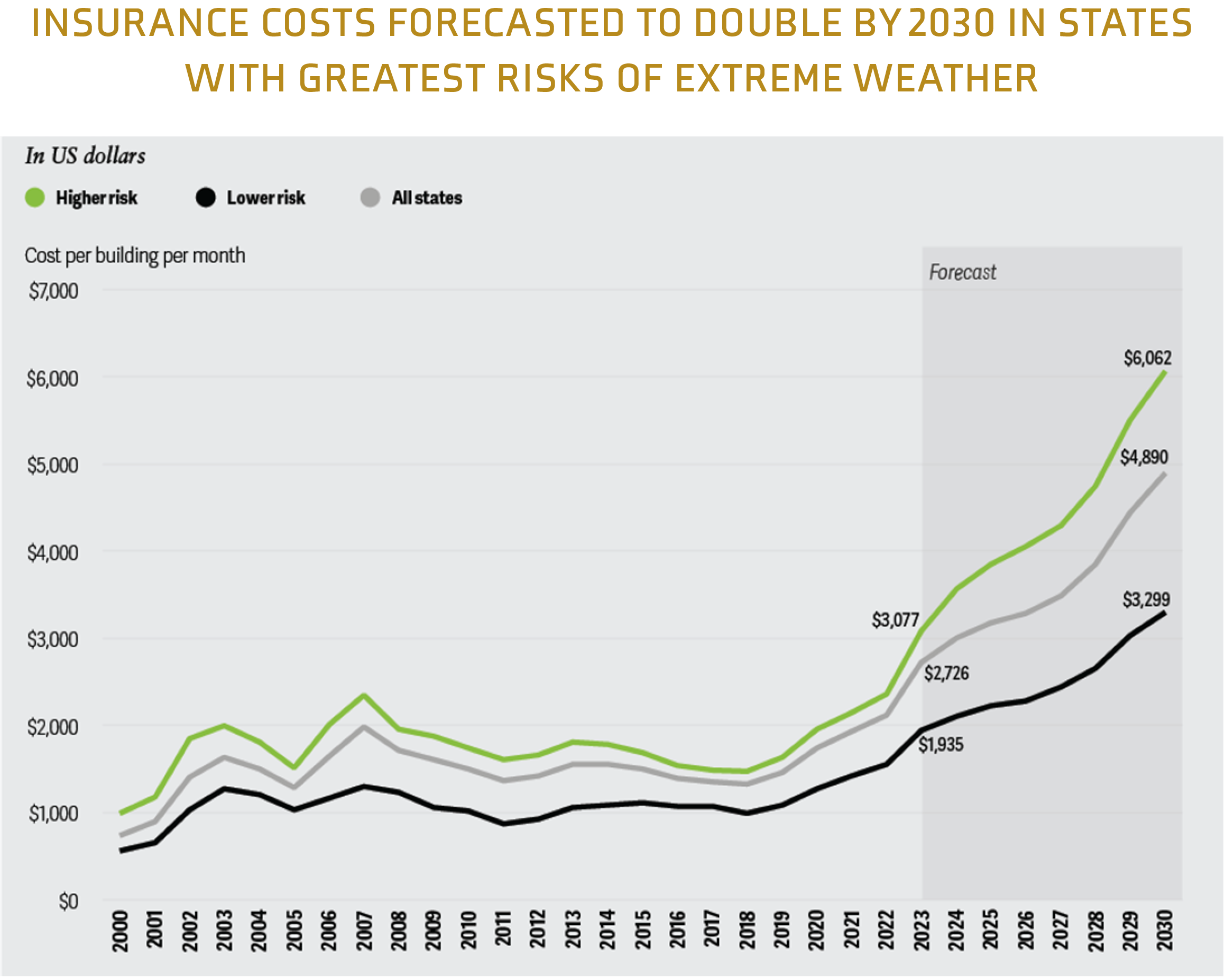

The start of 2025 has brought a continuation of climate-related and natural disasters. Wildfires in Southern California demonstrate that fire risks continue to grow with the potential for more significant losses. Total property and capital loss estimates for the Los Angeles-area fires could range from $95 billion to $164 billion, with insured losses estimated at $75 billion.1 This event is the most destructive wildfire in Los Angeles County history and potentially the costliest in U.S. history.2 Wildfires in urban areas and inland hurricane flooding in North Carolina from Hurricane Helene illustrate the expanding impacts of catastrophic events. Over the past five years, there have been an average of 18 natural disasters per year that cost at least $1 billion.1 The effect on residential property is well documented, but the impact on commercial property also presents challenges, where estimates for monthly average commercial insurance rates forecast to grow from $2,726 in 2023 to an estimated $4,890 in 2030. However, for states in extreme weather risk areas, rates are estimated to double, from $3,077 to $6,062.2

As property markets adjust, it continues to be a top concern for insurers heading into 2025, along with cyber threats, the environment, and climate.3 Insurers may need to weigh the quality of risk with the broadening of their premium volume in 2025.

Rising geopolitical tensions, such as the ongoing Russia-Ukraine conflict and unrest in the Middle East, continue to heighten risk assessments, particularly in cyber and marine exposure.4 These tensions, as well as proposed trade policies by the new presidential administration may contribute to market uncertainty, ultimately causing higher interest rates impacting earnings growth, investment asset valuation, and balance sheet shareholders’ equity.5 Deloitte points out that tariffs with Canada and Mexico will impact the cost of auto and homeowner claims could increase due to higher prices for aftermarket auto parts and construction materials.4

Source: Deloitte Center for Financial Services analysis of NCREIF data6

Market Outlook

According to S&P Global, premium rates for the P&C industry are expected to moderate as insurers will now focus on maintaining underwriting margins and expanding existing policies.5

Property

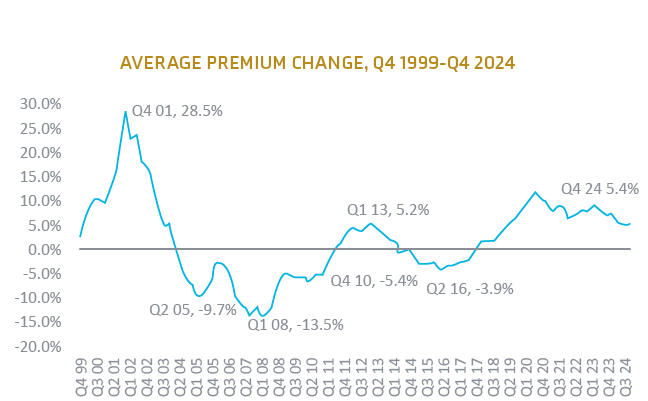

After a turbulent ride in 2023, the property and casualty (P&C) market stabilized throughout 2024,3 led by strong revenue and earnings.

In Q4 2024, commercial property premiums increased on average 6%, down from 7.9% in Q3 2024 and 11.8% in Q2 2024.7

The U.S. P&C market underlying growth is forecast to outperform overall GDP growth for the next two years, and replacement costs are expected to overtake overall inflation (3.3% vs 2.5%).8

Net written premiums for few carriers are seeing an increase in year-over-year changes. Chubb reports their year-over-year written premiums for the P&C market increased 7.7% from 2023 to 2024.9

S&P Global forecasts net premiums in 2024 and 2025 to grow at 8%-9% as insurers respond to elevated claims costs with moderate rate increases.7

According to a Nearmap analysis, Hurricane Milton caused property losses affecting over 234,960 properties. The total estimated loss was $54 billion, with $16 billion for insurers. Insured losses amounted to a $25 billion contribution to a total loss of $38 million.10

Premium increases resulting from the Los Angeles wildfires are expected to take several months to materialize. When they do, the market may face greater challenges, particularly as reinsurance renewals continue to recover from previous years. The impacts will likely be concentrated in specific regions, while the overall effects will be distributed across the industry.

General Pricing Estimates

Non-CAT exposed property with a favorable loss history

Down 1% to up 19%

CAT exposed property with a favorable loss history

Up 30% to 45%

Source: CIAB Commercial Property/ Casualty Market Index Q3 20247

Casualty

General Liability

Capacity is available and selective. Markets are implementing higher retentions and stricter terms, with prices increasing for frequency and rising costs.11

Submissions have increased and slowed due to increased capacity and additional consideration.Amwins. (2024, December 2024). State of the Market – 2025 Outlook.11

Excess Liability

Rates remain strong with a tightening of risk appetite.

Reinsurers are strategically managing capital allocation to safeguard their returns on liability lines.

Underwriting remains a priority, with an emphasis on improving risk distribution and maintaining healthy margins on liability lines.

General Pricing Estimates

General Liability

Flat to up 5.3%

Umbrella & Excess Liability

Flat to up 8.7%

Workers’ Compensation

Workers’ compensation realized an average loss cost decrease of more than 9% in 2024. Estimates expect a more modest reduction of 6% in 2025.12

Over the past year, lost time claim frequency declined 8%, reflecting a continued downward trend fueled by enhanced workplace safety measures. Ongoing advancements in safety technology have supported steady annual rate reductions across most U.S. states.

Job safety has been a higher priority than in past years as carriers favor risk mitigation efforts. While risk mitigation is favorable, when injuries do occur carriers are focused on a complete and rapid recovery remains a carrier priority.

Auto

Commercial auto remains unprofitable, with the direct incurred loss ratio through Q3 2024 being the second highest in 15 years.12

Personal auto pricing trends are moderating, and the sector’s 2024 combined ratio projection of 97.7% continues its improvement from 2022’s worst-in-decades combined ratio of 112.2 %.13

Stronger underwriting performance in personal auto is expected to drive the industry combined ratio for 2024-2025 to be 98%-100%.5

Electric vehicles are increasingly being integrated into commercial fleets, bringing significant risk liability. Their batteries present an even greater hazard, as they have a higher likelihood of catching fire and burning more intensely than combustion engine vehicles.14

Regions with frequent high nuclear verdicts, such as California and Texas, are expected to experience greater rate increases and reduced capacity.

GENERAL PRICING ESTIMATES

Workers’ Compensation

Down 1.8% to flat

Auto

Up 1% to 8.9%

Executive Risk

Cyber

The cyber threat continued to escalate in 2024, with increases in both the frequency and severity of claims.4

Cyber premiums decreased in Q4 2024 an average of 1.8%.7

Businesses across all sizes experienced rising claims frequency and severity. Those with under $25 million in revenue saw moderate increases, while mid-sized companies ($25 million to $100 million) faced a 32% rise in frequency and a 9% increase in severity.15

Directors & Officers (D&O)

The overall D&O market conditions remain favorable for early 2025.

The recent downward pressure on pricing has slowed, but capital remains plentiful and competitive.

The market is seeing new capacity (more supply) but less demand – the decline of IPOs and de-SPAC transactions, creating more competition for “legacy business.”

Carriers remain cautious with companies that have a high likelihood of being acquired or near-term capital needs.

Even with increasing litigation and IPO activity, it may take some time before pricing changes course.

There is cautious optimism for the current market trends for the foreseeable future.

GENERAL PRICING ESTIMATES

Cyber

Down 1.8% to flat

D&O liability

Down 1.5% to flat

Major Claims in the Sector

Personal Injury | Products Liability

$55.5 Million Verdict While using her pressure cooker, the plaintiff was injured with second and thirddegree burns when it exploded. A jury found the plaintiff only 10-percent responsible and awarded $55.5 million.16

Discrimination | Employment & Labor

21 Million Verdict The plaintiff worked for 21 years as a clinic’s medical director. He resigned in 2020 after accusing the hospital of institutional racism and retaliation after pointing out his concerns. Jurors awarded $21 million.17

Wrongful Conviction

$34 Million Verdict The plaintiff spent nearly 16 years in prison for a murder she did not commit. Jurors awarded $34 million.18

Guidance

Begin the process early.

Partner with your broker early to prepare for any changes to increase greater renewal success.

Partner with industry experts.

It is important to work with your broker’s industry experts who understand the business and the market for placing the specific risk. Collaborating with a team that can best represent your risk and partner with your operations is more critical than ever in this disciplined market we are experiencing.

Highlight cyber security and proactive risk management.

IMA has a team solely dedicated to managing cyber risks. They offer expert assistance, including coverage analysis, financial loss exposure benchmarking, contract language review, in-depth cyber threat analysis, and strategic development of comprehensive, high- value cyber insurance programs.

Review your contracts.

Our contract review teams add value to our clients’ overall risk management program by ensuring the indemnity language is market standard and doesn’t expose our clients to unforeseen losses that may not be insurable.

Contact

Jason Patchen

SVP, National Director of Carrier Relationships

Vasile, N. and West, Z. (2025). Cyber Premium Relief Continued While Auto Struggled for 54th Quarter, The Council’s P/C Market Survey Shows. Commercial Property/Casualty Market Index Q4 2024. Council of Insurance Agents and Brokers. https://www.ciab.com/resources/q4-2024-p-c-market-survey/↩︎

Tyson Mendes Nuclear Verdicts. (2024, December 13). $55.5M for CO Woman After Pressure Cooker Exploded, Burning Her. Tyson Mendes. https://www.tysonmendes.com/cases/↩︎

Tyson Mendes Nuclear Verdicts. (2024, December 24). $21M for WA Doctor After Racial Discrimination at Work. Tyson Mendes. https://www.tysonmendes.com/cases/↩︎

Tyson Mendes Nuclear Verdicts. (2024, December 13). $34M for NV Woman After Almost 16 Years Incarcerated Due to Wrongful Conviction. Tyson Mendes.https://www.tysonmendes.com/cases/↩︎