Real EstateInsurance Pricing & Market Update

Q4 2024

The real estate market has weathered record storms and uncertain economic conditions and appears to be stabilizing. Slower inflation and moderating interest rates may provide the tailwinds to usher in positive opportunities in 2025 even as a wide range of variables look to impact availability of capacity, breadth of coverage, and competitiveness of rate.

Rate increases over the past couple years have put carriers and reinsurers in good position, and price moderation is expected in 2025 except for auto and excess lines. Reinsurance capacity continues to increase and demand for reinsurance coverage is also growing.1

Even though the 2024 hurricane season had several impactful storms the catastrophic damage was less than anticipated and unfortunately uninsured in some areas. Milton caused less damage than forecast and investors in catastrophic bonds experienced little impact from the storm.2 The Swiss Re global cat-bond index is up more than 13%, as investors emerge largely unscathed after what meteorologists had warned would be one of the most active hurricane seasons in recent memory.

Overall construction starts slowed even as spend increased. Year-over-year construction starts are down 8.3 percent, led by non-residential at 33.4% while residential was down 16.2%.3 Residential single-family and manufacturing sectors led the industry, but multi-family and commercial were down, and both are expected to continue to taper off into 2025. Contractors of all sizes have experienced a decline in backlogs, now at 8.4 months and a 0.9 month decrease year-over-year.

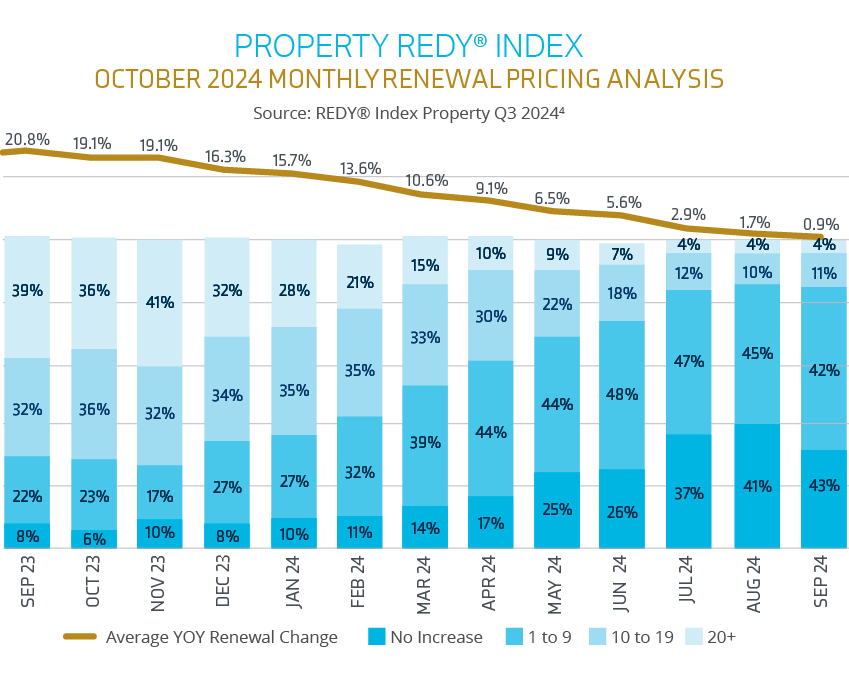

There is no shortage of capacity for property as the reinsurance market signals more capacity, backed by strong third-party capital and supported by securities.

| Non-CAT exposed property with a favorable loss history | Down 10% to up plus 5% |

| CAT exposed property with favorable loss history | Down 2% to up plus 5% |

General Liability

Excess Liability

| General Liability | Up 5% to 10% |

| Umbrella & Excess Liability | Up 10% to 15% |

Workers’ Compensation

Auto

| Workers’ Compensation | Down 2% to Flat |

| Auto | Up 10% to 20% |

Cyber

Jim Litterer

EVP, National Real Estate Practice Director

Crystal Kohnert

SVP, National Accounts Director – Real Estate

Angela Thompson

Sr. Marketing Specialist, Market Intelligence & Insights

Brian Spinner

Sr. Marketing Coordinator, Market Intelligence & Insights