How Employers Can Help Employees Prepare for Retirement

Jul 16, 2026

Retirement is a significant milestone for all employees that most often requires careful planning. Unfortunately, many employees have fallen behind in either setting realistic, achievable goals for their retirement or had trouble maintaining the goals set. Increasing financial pressures make retirement planning more difficult. Cost of living increases, student debt, and low salaries can overwhelm efforts of employees to adequately save for retirement. A central driver, according to the TIAA Institute’s 2025 Future of Retirement Security report, is the broad shift away from Defined Benefit (DB) plans – which guaranteed workers a reliable income in retirement – toward Defined Contribution (DC) plans, which accumulate savings but do not automatically convert into income.1 This structural change has placed the burden of retirement planning squarely on the individual employee. Additionally, employees are putting off saving for retirement to focus on current financial needs and expenses, believing they will be able to compensate for the delayed start at a later time.

For employers, creating a culture of retirement preparedness is not only a responsible business practice but also a vital contribution to the overall well-being of their workforce. Acting on this assessment, many employers are implementing strategies to assist employees in their effort to remain committed to their retirement savings and, in some cases, aid them in catching up if they have fallen behind.

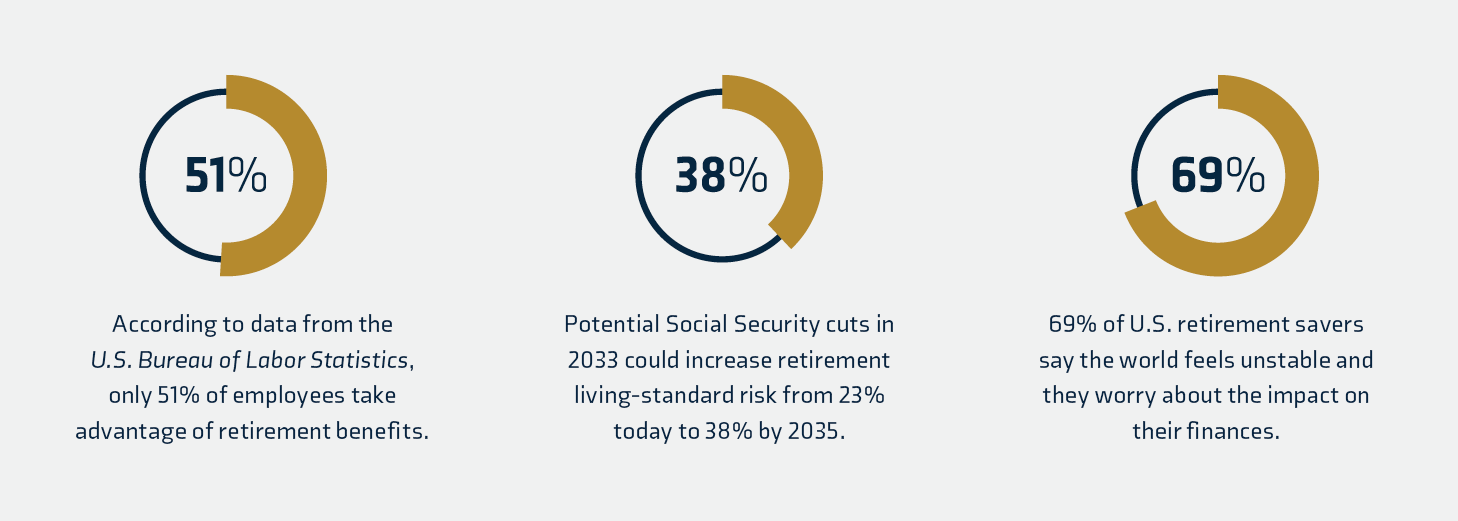

Over the last few decades, retirement has dramatically changed. In the past, workers could rely on their employer to provide them with income as they aged, but now workers must leverage personal savings and other benefits, such as Social Security, to provide for a reasonably comfortable retirement. According to a 2025 report by research firm Valoir, nearly 80% of employees say financial wellbeing is at least a moderate source of stress — and finances remain the single biggest stressor employees report in the workplace.2 Despite these concerns, only 51% of employees take advantage of retirement benefits offered by their employers, according to data from the U.S. Bureau of Labor Statistics.

While inflation has moderated since its 2022 peak, persistently elevated costs of living, ongoing economic uncertainty, and concerns about Social Security’s long-term solvency continue to create barriers to a sufficient level of retirement savings. This last point is particularly pressing: the TIAA Institute warns that Social Security faces potential benefit cuts as early as 2033, which could increase the share of retirees at risk of declining living standards from 23% today to 38% by 2035. Workplace retirement plans are becoming correspondingly more critical as the necessary foundation for retirement security.

Compounding these pressures is the fact that most Americans are now living longer. According to the Centers for Disease Control and Prevention, the American life expectancy from birth has risen from 47.3 years in 1900 to 79.0 years in 2024. The TIAA Institute presents this in even sharper relief: the average retiree today can expect to spend about two decades in retirement – nearly double the retirement period 50 years ago. In the United States, specifically, men can expect an average of 18 years in retirement and women 20.6 years. The extended life spans mean retirement funds must stretch further than at any point in recent history.

For many employees, the path to a secure retirement still feels uncertain. According to the 2025 Natixis Global Retirement Index, while optimism concerning a secure retirement among Americans has improved, 69% of U.S. retirement savers say the world feels unstable and they worry about the impact on their finances.3 Globally, 43% of those currently investing in their retirement still say it will take a “miracle” to retire securely — a sobering reminder that retirement readiness remains a pressing concern even as investment confidence rises.

In response to employee anxiety concerning their future, there are several strategies organizations are employing to help their workforce prioritize and prepare for retirement.

Employers can educate employees on topics such as budgeting and emergency savings accounts to help them save for retirement. This education is more urgent than it may appear: the TIAA Institute’s 2025 report found that only 12% of adults demonstrate strong longevity literacy — meaning most employees lack a basic understanding of how long their retirement may actually last and the financial risks that accompany retirement. Educational efforts that include graphical depictions of retirement savings, personalized financial projections, and guidance on life expectancy can help employees understand how prepared they really are and motivate them to close any gaps that might exist between savings rates and projected retirement needs.

Some organizations offer employees access to financial experts and advisors. These professionals can provide individuals with critical insights into how prepared they are for retirement, as well as offer multiple strategies to help them accumulate retirement savings.

Employers can educate employees on retirement savings recovery opportunities and encourage them to take advantage of all available options. Currently, individuals aged 50 and older can make additional recovery contributions to their retirement accounts. Under SECURE 2.0, employees who earned more than $150,000 in FICA wages in 2025 are now required to make catch-up contributions as Roth (after-tax) contributions beginning in 2026. Additionally, employees aged 60–63 can take advantage of a higher “super” catch-up contribution limit of $11,250 for 2026 — a meaningful opportunity for those in the final stretch before retirement to accelerate their savings.

Additionally, employers can demonstrate to employees nearing retirement how contributing a higher percentage of their salary to a retirement plan, such as a 12%–15% increase, can help them meet their financial goals.

Flexible retirement options allow employees to tailor their approach toward retirement savings to their goals and lifestyles. A more personalized strategy may include target-date funds, nonqualified deferred compensation plans, and other investments, including venture capital, private equity, and real estate. The TIAA Institute’s 2025 report highlights a growing area of opportunity here: integrating guaranteed lifetime income options (such as annuities) directly into Defined Contribution (DC) retirement plan menus. Currently, only 2.4% of United States retirement assets are held in annuities, suggesting significant room to close what the report calls “the guarantee gap.” Employers who explore hybrid options – combining the growth potential of DC plans with the income security of guaranteed products – are better positioned to help employees not just save for retirement, but live securely through their retirement. Some employers have also established plans that automatically increase employee contribution rates over time, helping workers build savings steadily as they approach retirement.

Providing employees with regular communication regarding retirement benefits and options can often encourages greater participation. For example, Microsoft has achieved participation rates of over 90% in its 401(k) program by targeting its enrollment outreach only to individuals who have not yet signed up. Simple nudges such as this can have a measurable impact.

Sometimes, employees do not contribute to retirement programs because they must focus their finances elsewhere. For example, many employees must spend their money on caregiving instead of contributing to their retirement accounts. If an organization were to consider providing employees with voluntary benefits — such as caregiving benefits — that address their immediate needs, it would empower them to redirect resources toward their retirement savings.

Some employers offer profit-sharing plans that allow employees to earn a bonus that is automatically contributed to their retirement savings plans when the organization achieves its annual financial targets and goals. These contributions can help employees build retirement savings while also incentivizing them to work toward their employer’s shared goals.

According to Fidelity’s 2025 Retiree Health Care Cost Estimate, a 65-year-old retiring today can expect to spend an average of $172,500 on healthcare throughout retirement – not including long-term care costs.4 Additional Fidelity research finds that one in five Americans has never considered healthcare costs when planning for retirement. Medicare alone will not be enough. Companies can help future retirees by providing HSA contributions and educating employees about how to effectively use their HSA accounts as investment and retirement vehicles.

A one-size-fits-all approach to retirement is no longer a workable solution for most employees. As the TIAA Institute notes, the goal of a well-designed retirement plan is to help workers not just save for retirement, but live securely through it, which is a distinction that takes on new weight as retirement is now consisting of two decades or more. Employers have a unique opportunity to create a positive impact on the lives of their employees by taking proactive steps to assist them in preparing for retirement. Empowering retirement readiness can not only help employers improve their recruitment and retention efforts, but also demonstrate the company’s commitment to their employees’ well-being.