HealthcareMarket Update

Q2 2026

The healthcare insurance market is going through a lasting shift. Insurers are rewarding organizations that manage risk well and applying pressure to those that do not. Property insurance has improved for strong risks, but most liability lines remain challenging. Healthcare professional liability (HCPL) rates continue to rise by single digit rates, driven by larger claims rather than more frequent ones. Cyber remains concerning, with healthcare the most targeted industry,1 but rates are easing. Sexual abuse and misconduct coverage has become one of the most constrained and complex parts of the market.

Across all lines, insurers are no longer offering standard terms to all buyers. Pricing, limits, and coverage now depend heavily on how well an organization shows strong governance, prevention programs, and disciplined risk management. Insurance is no longer just a way to transfer risk. It is a reflection of how leadership manages risk across the organization.

The commercial property market has improved after several difficult years. Capacity is increasing and rate increases have slowed, especially for organizations with good loss histories, accurate data, and well‐maintained facilities. Insurers are more willing to compete for well‐performing risks, showing signs of a modestly softer market.

This improvement is uneven. Organizations in catastrophe‐prone areas, including wildfire, hurricane, and flood zones, continue to face tighter limits and higher pricing. Location, building condition, and mitigation efforts remain key drivers of underwriting decisions. Investment in facilities, accurate property data, and consistent loss control directly affect pricing and available capacity.

Casualty insurance conditions remain difficult across healthcare. Professional liability and sexual abuse coverage continue to tighten, with higher premiums, larger retentions, and reduced limits. Cyber insurance availability has improved, but insurers remain cautious and selective.

Across all liability lines, insurers are placing greater focus on high‐severity risk. Coverage is increasingly tied to governance, leadership oversight, and prevention efforts, not just claims history.

The HCPL market remains firm, with little expectation of near‐term relief. Pricing pressure continues even for organizations with improving patient safety outcomes. The main driver is claim severity. While claim frequency has stayed relatively stable, large verdicts and settlements continue to push total costs higher.

Organizations with weak loss histories or limited leadership involvement should expect sharper rate increases and closer underwriting review. Insurers are favoring providers that show strong governance, active claims oversight, and early intervention when incidents occur.

Cyber insurance capacity has improved for healthcare organizations that have invested in stronger security controls. Even so, cyber risk remains one of insurers’ top concerns. Healthcare continues to experience frequent attacks due to legacy systems, complex networks, and reliance on third‐party vendors.

Insurers are acting with tighter policy language, higher underwriting standards, and deeper reviews of security practices. Long‐term access to coverage depends on healthcare‐specific controls, vendor oversight, executive oversight, and tested incident response plans.

| Premium Changes in Other Lines | 4Q25 | High | Low |

|---|---|---|---|

| Business Interruption | -0.7% | 28.8% | -10.2% |

| Cyber | -3.3% | 34.3% | -3.3% |

| D&O Liability | -3.8% | 32.4% | -8.7% |

| Employment Practices | -2.6% | 21.9% | -8.1% |

| Flood | 1.0% | 8.6% | -2.7% |

| Medical Malpractice | 1.4% | 32.5% | -4.1% |

Source: CIAB Commercial Property/Casualty Market Index Q4 20252

Insurance now plays a different role in healthcare risk management. It is one part of a broader risk financing strategy that includes prevention, governance, and accountability. Organizations that cannot demonstrate risk maturity are seeing fewer options and less favorable renewal terms.

Insurance now plays a different role in healthcare risk management.

Insurers are increasingly separating healthcare buyers based on the strength of their risk programs. Key factors include executive ownership of risk, use of enterprise risk management frameworks, data quality, and consistent prevention efforts.

Insurance outcomes increasingly reflect leadership involvement. Organizations with mature risk profiles are realizing better terms and broader coverage, while those with weaker profiles or significant loss histories see higher rates, reduced limits, and more exclusions.

Uncertainty around federal reimbursement continues to strain healthcare finances. Questions remain about reimbursement for emergency care provided to uninsured individuals. Any reduction in funding would place added pressure on hospital margins, especially for safety‐net providers, which could impact liability exposure.

Healthcare staffing conditions look to be stabilizing, though there continues to be an imbalance between rural and urban areas. Staffing levels are closely linked to patient safety and care quality, which affect liability lines including professional liability, workers’ compensation, and medical malpractice. Over time, continued staffing improvements can help reduce rates increases, though the effect is likely to be gradual.

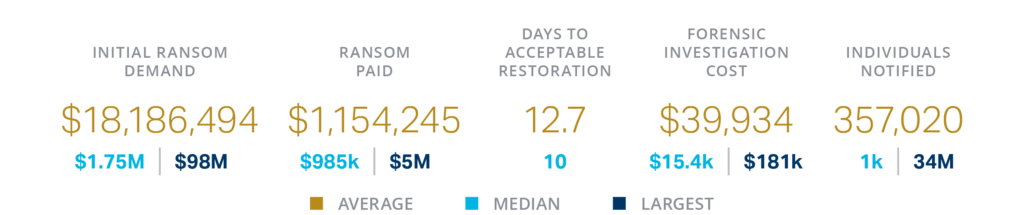

Healthcare remains the most targeted industry for cyber incidents. Attack frequency surged in the past year with phishing attacks accounting for nearly one‐third of all attacks. Vendor relationships remain a key vulnerability, with several major incidents originating outside provider systems.

Losses have increased year‐over‐year, driven by greater ransomware demands and payments. The cost of a breach extends well beyond system restoration. Regulatory scrutiny, notification requirements, and class action lawsuits often follow quickly, making cyber incidents among the most expensive events organizations face.

Source: Baker Hostettler 2026 Data Security Incident Response Report3

AI use is expanding across healthcare operations, including diagnostics, imaging, operations, and analytics. These tools offer clear benefits but also introduce new risks. AI raises concerns related to data privacy, regulatory compliance, and accountability when errors occur.

AI also affects cybersecurity. While it improves threat detection, it also enables more advanced attacks. Insurers are paying closer attention to how AI tools are governed and monitored.

Sexual abuse and misconduct (SAM) coverage has become one of the most difficult lines of healthcare insurance. Capacity is shrinking, premiums are rising, and policy terms are changing quickly. Large settlements and expanded statutes of limitations have made these claims harder to predict and more expensive.

Insurers are limiting exposure through lower sub‐limits, higher retentions, and broader exclusions. Embedded SAM coverage is often being replaced by standalone policies with narrower terms, and a growing number of carriers are excluding SAM entirely unless providers meet strict underwriting guidelines.

Several trends are reshaping this coverage landscape. A growing number of states have extended or eliminated filing deadlines for abuse‐related civil claims, which may allow for decades‐old incidents to surface in litigation. Because many carriers historically wrote these policies on an occurrence basis, they are now absorbing losses tied legacy occurrence based policy periods written decades ago. Nuclear verdicts and third‐party litigation financing are enabling claimants to pursue lengthy, costly cases, which helps to escalate settlement costs.

Meanwhile, exclusions are growing broader and some carriers are splitting physical and sexual abuse into separate categories and sub‐limiting them.

Access to SAM coverage now depends heavily on prevention maturity. Insurers are closely reviewing:

Organizations that demonstrate consistent prevention practices, strong organizational culture, and leadership oversight are better positioned to secure coverage.

Prevention is more than a policy document — it is a daily organizational commitment. Organizations that treat SAM prevention as a compliance exercise rather than a cultural priority will find themselves increasingly disadvantaged in the insurance market and increasingly exposed when incidents occur. Key practices include:

The defining trend in healthcare liability claims is rising severity. Average claim costs continue to increase by about 6% per year, even as claim frequency remains steady. Over time, this drives higher premiums, larger retentions, and more restrictive coverage.

Insurers are focusing on how organizations manage claims early and prevent escalation. Early intervention, disciplined litigation management, and clear settlement authority are key underwriting considerations.

The current healthcare insurance market clearly favors organizations that treat risk management as a strategic priority. Coverage terms, pricing, and capacity increasingly reflect leadership behavior, governance strength, and prevention culture.

Organizations that invest in strong controls, executive ownership of risk, and disciplined risk financing are better positioned to secure stable coverage and manage long‐term costs. Those that view insurance as a procurement exercise rather than a leadership responsibility face higher premiums, reduced capacity, and growing uncertainty.

In today’s market, risk maturity is no longer optional. It is a competitive advantage.

Ryan Roberts

SVP, National Healthcare Practice Leader

Annie Nason

Vice President, Claims

Autumn Stone

Account Executive, Cyber Risk Solutions

Angela Thompson

Marketing Strategist, Market Intelligence & Insights

Brian Spinner

Marketing Specialist, Market Intelligence & Insights