Energy Market Update

Q1 2026

This Q1 2026 edition of Energy Markets in Focus provides a data-driven view of the underwriting, pricing, and coverage trends shaping today’s energy insurance market. Across upstream E&Ps, oilfield service contractors, midstream systems, chemicals and ethanol operations, and emerging power and IPP developers, the first quarter of 2026 continues to be defined by shifting capacity dynamics, heightened scrutiny of operational reliability, evolving environmental liability interpretations, and a heightened focus on loss-severity drivers.

Recent geopolitical developments involving Iran have reinforced the market’s sensitivity to supply disruptions affecting key global energy corridors and producers; even short-lived interruptions involving material contributors to oil and LNG supply (such as the early-March halt reported in Qatar) can drive price volatility, logistics uncertainty, and insurance repricing considerations across property/BI, marine, and executive risk.

These insights reflect work with publicly traded enterprises, diversified private operators, and PE-backed platforms managing multi-asset, multi-risk portfolios. This vantage point allows us to focus not only on what the market is doing— pricing movements, limit behavior, wording adjustments, environmental constraints, and developing loss patterns—but also on how organizations can proactively respond. The emphasis is on the practical levers that help clients outperform the market, strengthen underwriting confidence, and improve terms through credible, evidence-based risk positioning.

The objective is to deliver market intelligence enhanced by actionable, technically grounded risk-management guidance that helps energy leaders anticipate trends, influence underwriting outcomes, and build more resilient risk and insurance strategies for the year ahead.

Recent developments in the Middle East have underscored how quickly disruptions involving major energy suppliers can influence insurance exposures. Early-March interruptions to LNG production in the region and periodic constraints around key shipping corridors highlighted how fast volatility can translate into supply-chain stress, price movement, and underwriting reassessment across several lines.

Higher commodity prices and tighter logistics are elevating property and business interruption (BI) exposures in ways that can outpace declared values and gross margins.

Marine and transit exposures are moving in parallel with geopolitical developments, with war-risk pricing and routing changes creating new layers of complexity.

Operational and contractor risk can rise when commodity strength accelerates activity.

Political violence and war-risk terms are under renewed scrutiny for organizations with overseas assets or international exposures.

Executive and board-level risk also increases in volatile periods.

Overall, geopolitical volatility is directly influencing underwriting behavior across property, BI/CBI, marine, casualty, and executive risk. Clients should expect deeper questions on values, supply-chain dependencies, contractor controls, and governance, and be prepared to align program structure and documentation accordingly.

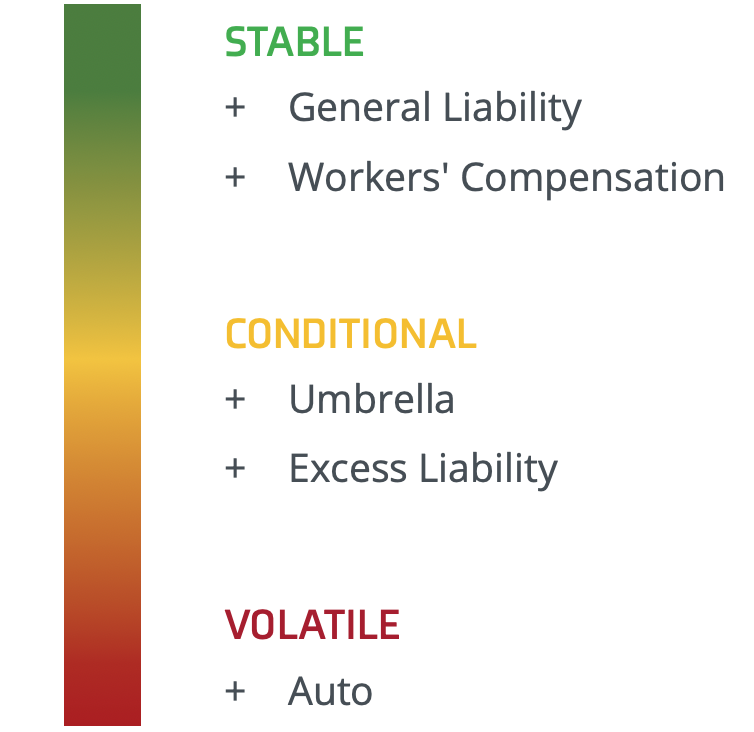

Property insurance for the energy industry continued to soften, supported by a favorable reinsurance backdrop, but liability conditions remain uneven, particularly in the domestic market for auto and workers’ compensation coverages.

For well-engineered midstream and chemical accounts with clean loss histories, rate decreases of approximately 15% are achievable. General liability (GL) and workers’ compensation (WC) are flat to negative, and umbrella is manageable where competition is introduced. Auto liability remains the clear exception. Renewals in West Texas are significantly higher year-over-year, with some insurers exiting the market altogether. For property coverage, rates are flat to slightly down, though markets continue to push for business interruption (BI) volatility clauses, making accurate reporting more critical than ever.

Some localized constraints remain. In Louisiana, pre-existing conditions coverage for upstream assets is nearly unavailable, with most markets now resetting retro dates annually. Meanwhile, select carriers are expected to re-engage traditional oil and gas risks later in 2026, which could introduce useful new competition at renewal.

London is in an aggressive growth mode, with more capacity and better pricing than a year ago across most energy lines. The most notable shift is London’s push into middle-market accounts, where they have historically competed only on larger deals. Direct London markets are willing to reduce minimum premiums on general liability and excess placements, looking to compete with managing general agents (MGAs) and domestic markets for growing or newer businesses.

London is taking larger positions and sitting lower in excess towers than in recent years. Rate decreases of 5–15% on direct London placements are common for control of well (CoW), oil and lease (OLP), and midstream property.

For primary GL, London is actively competing and offering more capacity than previously available. Fracking exposures remain the exception—a challenge for both London and domestic markets—but E&P, midstream, manufacturing, and contractor risks are seeing strong competition.

For primary and lead excess placements, London markets are increasingly requiring advanced planning before quoting. For serious engagement, this step is becoming non-negotiable.

The single most influential factor in contractor performance is pre-job planning, which can optimize operational productivity and mitigate risks, or it can negatively impact downstream controls. Markets are looking for planning by, and between, operators and contractors.

Several converging trends are elevating risk on the midstream and infrastructure side. Aging infrastructure operating beyond its original design life and without corresponding upgrades to inspection or condition-monitoring programs increases the likelihood of high-severity equipment failures. Contractor-driven maintenance and modification work introduces additional exposure when temporary configurations are not fully captured through the management of change process. Facilities with high contractor activity do not always formally account for Simultaneous Operations (SIMOPS) risks, which require structured risk assessments to ensure contractors understand surrounding operations and potential escalation pathways.

The consistent theme across these trends: the gap between written programs and actual field execution remains the primary driver of contractor-related losses.

One counterintuitive observation from fieldwork: smaller operators often demonstrate stronger safety cultures than their larger counterparts. Because a single significant loss can be existential for a small firm, ownership of safety tends to run deeper, and leadership is closer to the work. Larger organizations sometimes absorb incidents in ways that dilute accountability. These cultural dynamics never appear in submission documents, which is why field-level visibility is important for evaluating contractor risk.

Traditional well control frequency has declined meaningfully over the past decade, driven by advanced interlock and automation systems and improved procedural discipline around startups, shutdowns, and pressure control. Together, technology and behavior have produced the largest reduction in high-severity events.

The most significant shift in control of well exposure is where loss events are actually occurring. Historically, drilling and completions carried the highest blowout risk, but field data now clearly point to plug and abandon (P&A) operations as the primary source of well control events. Many P&A wells involve poorly documented histories, unexpected pressure pockets, compromised casing or cement integrity, and crews unprepared for full well control contingencies. This pattern is underreported in submission documents and largely underappreciated by underwriters.

Closely related is the growing concern around orphan and zombie wells. Older wells drilled with inadequate casing can create unexpected communication events when new drilling or completions occur nearby. Recent losses are raising concerns with underwriters due to the long-term, open-ended nature of the exposure created.

Three factors consistently drive loss severity in control of well events:

Control of well pricing in London has been competitive, but several notable losses in 2025 may prompt a market correction in late 2026 or into 2027. More broadly, non-competition buybacks are rising, and double-digit rate increases have been consistent. There are also concerns that some London markets are offering distressed accounts terms that appear too favorable given the underlying loss history, a dynamic worth monitoring.

Across E&P, contractors, midstream, and chemicals, liability severity is the dominant theme—driven by litigation inflation, nuclear verdict exposure, and environmental claims. On the property side, losses remain impactful but increasingly segmented by asset quality and risk engineering.

In E&P, well control events, aging infrastructure failures, and contractor losses involving heavy equipment continue to result in significant losses. Auto and umbrella liability severity is rising sharply, fueled by aggressive litigation, action- over suits, and environmental spill exposure.

In midstream, compressor station failures, pipeline leaks, and environmental contamination are the primary severity drivers.

In chemicals, large property damage and business interruption outages and process safety events have produced the market’s largest recent losses, while PFAS-related and regulatory-triggered pollution claims are pushing liability severity higher across the sector.

Business interruption remains the most misunderstood coverage area, with persistent disputes around waiting periods, trigger language, and the interaction between BI and availability guarantees or liquidated damages. Cost of well claims are increasingly tied to casing integrity issues, with ongoing disputes over whether remedial operations qualify as well control expenses or re-drill costs.

Sudden and accidental (S&A) trigger definitions and primary/excess disputes between S&A and pollution legal liability insurers remain unresolved friction points. A commissioning coverage gap also persists where new assets generating revenue may fall outside both construction and operational programs if delay in startup/advance loss of profits coverage has not been purchased.

Early adjuster engagement, contemporaneous operational records, and synchronized BI reporting templates consistently produce better outcomes. Telematics and sensor data are increasingly valuable in fleet and equipment-heavy claims. Delays in sharing regulatory notices—particularly cleanup orders— can significantly escalate environmental losses. Structured kickoff meetings between insured, adjuster, and broker at the outset of complex claims remain one of the most effective tools for aligning expectations and reducing friction. Clients should also maintain a bordereau of small or notice-only losses within their annual aggregate deductibles to avoid potential claim denials due to late notification.

Jury awards and settlement values are rising broadly, with plaintiff-friendly jurisdictions in Texas and Louisiana shaping attachment point strategy. Third-party litigation funding is enabling more filings and prolonging defense cycles. Environmental litigation, contractual indemnity disputes, and emerging climate-linked claims are the most relevant legal exposures for energy clients. A front-loaded defense strategy—early counsel engagement, robust damages challenges, and strategic mediation— is increasingly essential to prevent cases from escalating into portfolio-shaping verdicts.

Data-center construction across the southern United States, particularly from Dallas through west Texas, is accelerating at an unprecedented pace.1 Texas has added 43 data center projects above 100MW since 2023, and only seven before then.2 This expansion is occurring against a backdrop of increasing grid stress, particularly across ERCOT, creating a risk profile outgrowing traditional property and casualty (P&C) underwriting models.

A growing number of projects are incorporating behind-the-meter generation specifically because grid interconnection timelines are uncertain or delayed, and many are structured with long-term offtake arrangements tied directly to hyperscale tenants, which reduces merchant exposure but increases dependency on single-customer reliability commitments. Several new power generation concepts are being reconfigured to scale down both scope and power requirements as developers refine economics and grid assumptions. Additionally, some projects are being financed directly by technology companies rather than through traditional PE structures, reflecting hyperscalers’ interest in securing dedicated generation capacity.

Long lead times for critical equipment remain the primary driver of delay in start-up exposure. Tenant energization milestones are often contractually fixed, meaning delay penalties can be substantial if commissioning timelines slip. London markets are showing strong appetite for large-limit layered builders’ risk programs that include early risk engineering engagement and equipment lead-time analysis. A growing trend in program structure is combining builders’ risk and first-year operational policies into a single integrated placement, providing seamless coverage through the transition from construction to operations.

Engage risk engineering during the development phase. Early identification of single points of failure, spare equipment strategy, and protection scheme reliability consistently improves both placement outcomes and long-term operational flexibility. Involving a broker and carrier in design review before construction begins has long-term implications on insurability and premiums that are difficult and costly to reverse. Insurers are also increasingly focused on contingency planning for both critical equipment and key personnel, with succession planning at the operational level becoming a specific underwriting consideration for projects with concentrated expertise or single-operator dependencies. Management teams should also be prepared to navigate the interplay between OEM, PPA, lender, and EPC agreements, as misalignment across these contracts is a common source of uninsured exposure.

Insurance Considerations for Active Buyers and Portfolio Operators

Private equity activity in the energy space remains active across upstream, midstream, power, and renewables, spanning both greenfield builds and asset acquisitions from larger peers.

Quality due diligence integrates risk engineering, valuation, and insurance review before deal pricing is finalized. Key red flags include fragmented programs with multiple brokers, misaligned renewal dates, outdated asset valuations that create under insurance exposure, deferred maintenance, large open claims, and historical pollution activity.

From closing through the hold period, the goal is a scalable program that absorbs add-on acquisitions at pre-agreed rates. Environmental tail structures should be customized to the PSA rather than treated as standard — explicitly allocating retained versus transferred liabilities can produce material savings for both parties. Insurance program quality and HSE investment relative to a go-forward strategy can also directly affect enterprise value. When programs are not fit for purpose, deal pricing should reflect it.

Current market conditions create both opportunity and risk at renewal. Capturing the opportunity requires preparation.

Underwriters are requiring more lead time than in prior years. New exclusions are appearing with increasing frequency, and additional marketing beyond initial plans may be required. Starting the renewal process early creates room to explore alternative market leaders and avoid being squeezed by underwriter capacity constraints at the last minute.

Insurers are scrutinizing auto risk management controls more heavily than ever. Clients should have a clear position on vehicle monitoring cameras before renewal— some insurers are now declining risks without them or a committed installation plan. A written cell phone and vehicle use policy, active MVR monitoring, telematics, and documented driver criteria enforcement all strengthen the submission. CAB reports should also be reviewed and corrected well in advance of renewal.

Before quoting, underwriters are now researching accounts—reviewing websites, social media, and CAB reports. Clients should audit their public presence to ensure it accurately reflects their operations and remove outdated or inconsistent content. Any loss with a hint of severity needs a clear explanation and a documented loss control response. A well-organized loss history with a credible remediation narrative consistently produces better underwriting outcomes than the numbers alone would suggest.

Stephanie Crochet |SVP, National Energy Practice Leader

Landon Plumer | Executive Vice President, Energy

Grady Goode | Senior Vice President, Energy

Dan Jack | Executive Vice President, Commercial Lines

Watson Barker | Executive Vice President, Commercial Lines

Austin Struble | Vice President, Energy

Donnie Steil | Risk Control Practice Leader, Energy

Rob Pritchard | Claims Specialty Practice Leader, Energy and Marine

Sharon Burger | Senior Vice President, Environmental Practice

Dalveer Channey | Engineered Risk Control Leader

Brian Barger | P&C Leader, Private Equity and M&A

Andrea Krueger | Strategic Risk Advisor

Adam Teague | Account Executive, Energy

Bryce Cornejo | Account Executive, Commercial Lines

Carolyn Salapa | Account Executive, Commercial Lines

Clay Shepler | Account Executive, Commercial Lines

Nick Brown | Account Executive, Commercial Lines

Jordyn Arons | National Practice Director, Private Equity and M&A

Angela Thompson | Marketing Strategist, Market Intelligence & Insights

Brian Spinner | Marketing Specialist, Market Intelligence & Insights