The real estate industry has experienced turbulent swings in recent years. Market dynamics, including fluctuations in property values, poor economic conditions, and rising interest rates, have negatively impacted real estate clients. With economic downturns, there can be decreases in the need for additional commercial spaces such as retail centers, office buildings, and warehouses, but rarely habitational exposures. The real estate sector continues to grow in acquisitions and thirdparty management.

From ownership and third-party management to research, consulting, valuation, and asset management, the real estate industry encompasses a range of specialized activities. Revenue growth is expected as many habitational projects and commercial projects are completed and online. The housing shortage continues to be a driver. Improved economic conditions will help drive industry growth due to an increased demand for retail and multifamily habitational space. The industry needs to stay vigilant, considering high-interest rates that continue to influence commercial building demand, increases in construction labor costs, and a more complex insurance market.

Market Overview

Property

The greater need for facultative reinsurance has slowed the quoting process.

A leading carrier in property writing and purchaser of reinsurance has led the way for valuations over the last three years, prompting others in the market to follow.

Losses in catastrophe-prone areas continue to outpace reinsurance.1

Reinsurance treaties renewed in 2023 have seen greater retentions and single-digit rate increases.

Greater capacity and reinsurers are looking to grow in the space. This will allow the primary writers to grow.

Insurance-linked securities (ILS) – CAT bonds have set a record for the highest influx of capital any year at $15.4 billion. The record places the overall ILS market in 2023 at $42 billion.

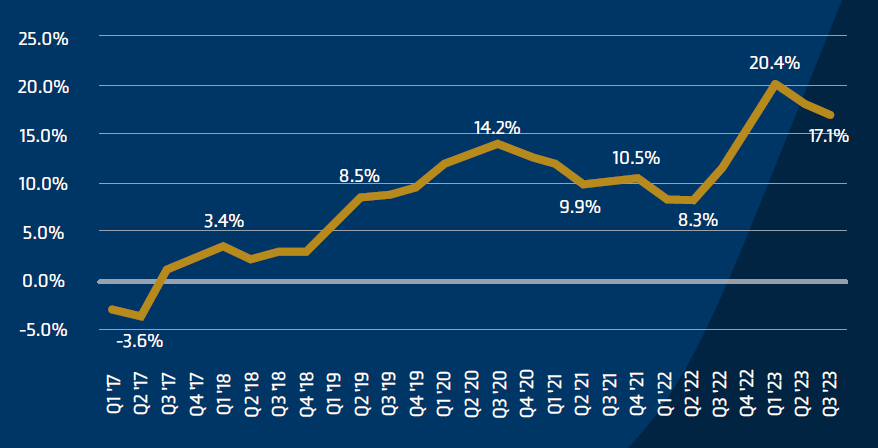

PREMIUM CHANGE FOR COMMERCIAL PROPERTY | Q1 2017-Q3 2023

General Pricing Estimates

Non-CAT exposed property with a favorable loss history

17% to 30% increases

CAT exposed property with favorable loss history

30% to 50% increases

Casualty

General Liability

General liability in the habitational space continues to be challenging, with 15%-30% rate increases for clean accounts and terms and conditions trailing slowly behind.

Aggregate limits are being managed by carriers by a reduction of half the annual aggregate. Unaggregated GL policies are rare to non-existent.

Insurers are also facing higher reinsurance costs and low investment returns, which are putting pressure on rates and causing an increase.

Depending on an organization’s risk profile and loss history, commercial general liability markets will likely experience increased premiums and stricter terms and conditions.

Excess Liability

Excess liability continues to be challenging as carriers follow the same approach as general liability, especially for high-difficulty and severity-prone risks.

Despite generally favorable conditions, many insureds are experiencing upward pricing trends due to inflation and heightened exposure in a growing economy. The challenging market conditions persist as carriers maintain restrictions on capacity and terms and substantial rate increases amid exposure expansion.2

General Pricing Estimates

General Liability

Up 15% – 30%

Umbrella & Excess Liability – Middle Market

Up 15% – 30%

Workers’ Compensation

Workers’ compensation coverage remains stable or unchanged in regions depending on job growth.

Workplace mental health data is growing. Stress and anxiety are now considered to be a top workplace injury, according to a study conducted by a Los Angeles-based law firm.3

Auto

The commercial auto industry has been struggling in hired and non-owned auto, with payouts from settlements and claims far outweighing profits.

General Pricing Estimates

Workers’ Compensation

Flat to 5%

Cyber

According to Corvus Insurance Q3 Report, 2023 Ransomware attacks are up more than 95% over 2022 and are predicted to remain consistent or increase through 2024.4

Additional capacity entered the market and underwriting standards have stabilized since the spike in claims from 2020 and 2021.

Organizations with strong security measures can anticipate positive ratings for cyber insurance renewals and look to negotiate coverage enhancements that were challenging to obtain in recent years.

General Pricing Estimates

Cyber

Flat to 15%

Major Claims In the Sector

Discrimination

$137M Verdict: A plaintiff suffered racial harassment at the workplace from a coworker and supervisor during their twoyear employment; he sued. Jury awarded $136.9 million.5

Habitability

$6M Verdict: A family moving into an older apartment discovered their child developed neurological issues due to lead paint, presumed due to the property’s age. The property also had a severe cockroach infestation. Plaintiffs, claiming non-disclosure of hazards and habitability issues, received a settlement of $6 million after disputing allegations of improper supervision and lack of hygiene.5

Contact

Jim Litterer

EVP, National Real Estate Practice Director