New Contraception Coverage Guidance

Sep 6, 2022

In response to the number of complaints the Departments of Labor, Health and Human Services (HHS), and the Treasury (collectively, the Departments) continue to receive, they have collectively issued a new set of frequently asked questions (FAQs) that clarify the requirements for contraception coverage under the Affordable Care Act’s preventive services coverage mandate. This most recent set of FAQs (Part 54) may be found here: https://www.dol.gov/sites/dolgov/files/EBSA/about-ebsa/our-activities/resource-center/faqs/aca-part-54.pdf

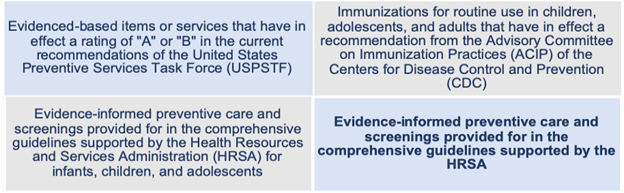

Under the Affordable Care Act (ACA), all non-grandfathered individual and group health plans are required to provide preventive services coverage with no cost-sharing. The list of preventive services required to be covered at 100% includes:

This list is updated by the appropriate departments/agencies over time. The requirements are summarized on Healthcare.gov – https://www.healthcare.gov/coverage/preventive-care-benefits/.

The HRSA guidelines include contraceptives.

The requirement for plans and carriers to cover items and service integral to the furnishing of a recommended preventive service also applies to coverage of contraceptive services under the HRSA-Supported Guidelines, including coverage for anesthesia for a tubal ligation procedure or pregnancy tests needed before provision of certain forms of contraceptives (e.g., an intrauterine device, or IUD), regardless of whether the items and services are billed separately.

As noted above, plans and carriers must provide 100% coverage of contraceptive products and services that are included in a category of contraception described in the HRSA-Supported Guidelines.

In addition, as previously clarified in FAQ part 51 guidance issued earlier this year (https://www.dol.gov/sites/dolgov/files/EBSA/about-ebsa/our-activities/resource-center/faqs/aca-part-51.pdf), plans and carriers must also cover products and services that are not included in a category of contraception described in the HRSA-supported guidelines if a provider has determined the product or service to be medically appropriate for the individual. NOTE – this includes products more recently cleared, approved, or granted by the FDA that may not be specifically included in the FDA’s Birth Control Guide referenced in the HRSA guidelines. Coverage must also include the clinical services needed for provision of the contraceptive product or service.

A substantial portion of the FAQs is devoted to clarification of appropriate medical management techniques and exceptions processes.

Medical Management Techniques

A plan or carrier may use medical management techniques:

Examples of unreasonable medical management techniques include things like:

Exceptions Process

Any exceptions process used must not be unduly burdensome (which is to be determined depending on the facts and circumstances) and must cover a service or FDA-approved, cleared, or granted product that a provider determines is medically necessary for an individual. The guidance outlines requirements for a transparent exceptions process:

Plans and carriers must cover FDA-approved emergency contraception, including emergency contraception that is available over-the-counter (OTC) when it is prescribed. The guidance also encourages plans to cover OTC emergency contraceptive products with no cost sharing when they are purchased without a prescription.

Current HRSA guidelines recommend “screening, education, counseling, and provision of contraceptives (including in the immediate postpartum period).” Counseling and education includes instruction in fertility awareness-based methods, including lactation amenorrhea for women desiring an alternative method.

A health savings account (HSA), health flexible spending account (HFSA), or health reimbursement account (HRA) can reimburse an individual for the cost (or portion of the cost) incurred for OTC contraception to the extent that cost is not paid or reimbursed by another plan or coverage.

Plans and carriers are encouraged (although not required) to cover the dispensing of a 12-month supply of contraception, such as oral contraceptives, without cost sharing.

Federal law preempts state laws that prevent coverage of contraception in accordance with the requirements of the preventive services mandate. While states have primary enforcement responsibilities for noncompliance by insurers, HHS will enforce the requirements if it believes a state has failed to do so. The FAQs also describe how the Employee Benefits Security Administration (EBSA) and Centers for Medicare and Medicaid Services (CMS) will work with plans as part of their regulatory oversight to ensure that plans are in compliance with the preventive services mandate as it applies to contraception.

Finally, the FAQ provides contact information for individuals who have concerns or complaints about how their plans are complying with the preventive services mandate.

Effective Date

The FAQ emphasizes that the most current HRSA guidelines were issued in 2019 and were recently updated in 2021.

Generally, plans must comply with updated coverage requirements one year after those updated recommendations are issued. Therefore, current plans should be in compliance with the 2019 guidelines and should begin complying with the 2021 updates for plan years starting on and after December 30, 2022.

Additionally, as noted above, it’s important to remember that plans and carriers must also cover products and services that are not included in a category of contraception described in the HRSA-supported guidelines if an individual and their attending provider have determined the product or service to be medically appropriate for the individual, including contraceptive products more recently approved, cleared, or granted by FDA.

Penalties for Non-Compliance

Violations may be subject to an excise tax under section 4980D of the Internal Revenue Code (Code) or a civil money penalty under section 2723 of the PHS Act (generally $100/day with respect to each participant to whom such failure relates) as applicable.

This latest set of guidance follows a recent letter issued by the Departments encouraging group health plans to full comply with the requirement to cover contraceptives with no cost-sharing. (See our alerts here and here)

As the Departments continue to receive complaints of non-compliance, and in light of the myriad issues facing both the preventive services mandate as a whole and the contraceptive coverage requirement in particular (i.e., the recent Supreme Court decision potentially making it more difficult to access abortions; continued questions about the extent of exemptions that apply to religious employers and employers with moral or religious objections to contraception; and another lawsuit challenging the constitutionality of the preventive services mandate now residing before a federal judge in Texas2); the Departments are working to make it as clear as possible what they expect from a compliance perspective and what potential penalties plans, carriers, and even states may face for failure to comply or enforce compliance with the law’s requirements as they stand today.

IMA will continue to monitor regulator guidance and offer meaningful, practical, timely information. This material should not be considered as a substitute for legal, tax and/or actuarial advice. Contact the appropriate professional counsel for such matters. These materials are not exhaustive and are subject to possible changes in applicable laws, rules, and regulations and their interpretations.