The outlook for senior housing is positive in the long run, with demographics working in the industry’s favor. The first of the baby boomers will be 83 in 2029 and the last turns 80 in 2047. In the short-term, however, owners and operators of these residences will need to weather challenges related to higher costs driven by labor availability, inflation, and higher interest rates offset in part by lower new construction rates relative to historic trends that will benefit existing communities.

Replacement costs have dramatically increased over the past several years, given the shortage of labor, higher building material costs and general supply line uncertainty. During these times of relatively rapid changes in replacement costs, it’s important for owners to keep pace with appropriate insurance limits to ensure adequate replacement costs.

As we learn to live alongside COVID-19, and the economy recovers along with the labor supply, senior housing property owners will be able to devote more attention and resources into innovation, amenities, differentiation, and customization – followed by scale. Experts warn, however, that generating benefits from scale in this industry is a tricky proposition, as consolidation and expansion come with the risk of damaging service quality.1

Due to higher interest rates and balance sheet pressure at regional banks, industry consolidation and merger and acquisition (M&A) activity will slow in 2023 from record levels in 2022.2 There is still plenty of room for consolidation, however, as the 50 largest companies in this space account for approximately 30% of the industry’s revenue.3

It’s important for owners to keep pace with appropriate insurance limits to ensure adequate replacement costs.

Coverage Outlook

Property

To mitigate the risk of being underinsured, businesses must take swift action to ensure their insurance replacement cost property valuations accurately reflect the increasingly higher costs associated with repairs and rebuilding, and adequately evaluate their exposure levels for business interruption losses.4 The sharp rise in prices, along with disruption to supply chains and labor shortages have caused these costs and lengths of time required to complete repairs and replacements to skyrocket.4

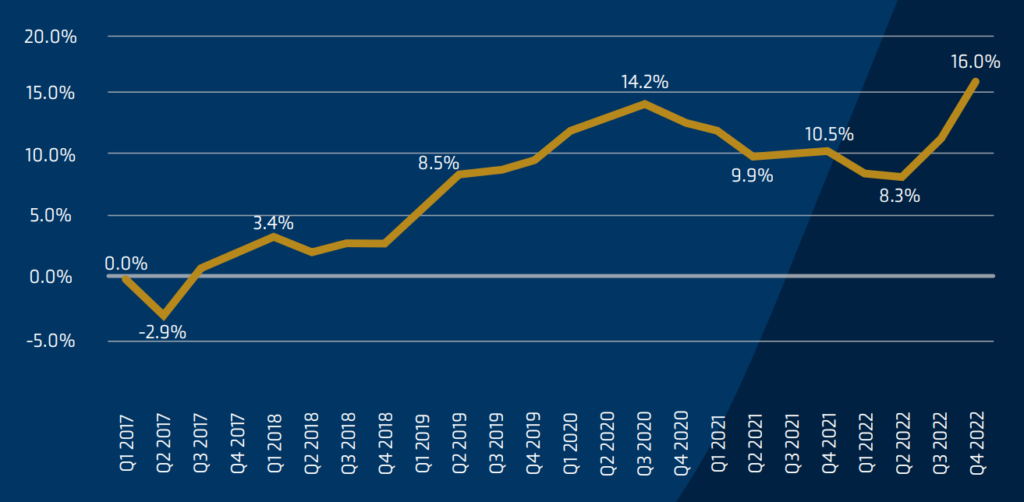

In Q4 of 2022, commercial property lines saw a remarkable surge in premiums, increasing by an average of 16%. This made it a standout among all other lines of business for this period.5

Natural catastrophes continue to be a leading cause of turbulence in the commercial property market.

Businesses must take swift action to ensure their insurance replacement cost property valuations adequately evaluate their exposure levels for business interruption losses.

PREMIUM CHANGE FOR COMMERCIAL PROPERTY | 2017-2022

Insurance to Value (ITV) is a top priority for carriers due to the escalating costs of commercial property. Mandates are being enforced that building values must be increased, particularly if they have not been adjusted in a while. This is to avoid potential losses, as in the case of any destruction or rebuilding, the insurer may need to pay out more than they would have prior to the value increase.4

Insurance to Value is a top priority for carriers.

GENERAL PRICING ESTIMATES

Non-CAT exposed with favorable loss history

10% to 15% increases

CAT exposed with favorable loss history

15% to 25% increases

Property with unfavorable loss history and/or a lack of demonstrated commitment to risk improvement (unresolved recs, pattern of same issues, etc.)

25%+ increases for non-CATASTROPHE

30% to 50%+ increases for CATASTROPHE exposed accounts and higher depending on frequency/severity of losses

Purchasers are in a more restrictive insurance situation.

Casualty

General Liability

Even though the primary general liability market is steady, purchasers are in a more restrictive insurance situation as insurers ask for more information detailing previous losses and the preventative measures taken to stop similar situations from occurring in the future.

Natural disasters such as hurricanes, earthquakes, or wildfires are continuing to have a substantial impact on the general liability market. These events have driven increases in property damage and bodily injury claims, leading insurers to reassess their underwriting strategies and pricing.

Excess Liability

The market is seeing carrier participation with smaller layers of excess liability coverage offered a bit more readily available year-over-year.

GENERAL PRICING ESTIMATES

General Liability

Up 5% to 10%

Umbrella & Excess Liability – Middle Market

Up 10% to 25%+

Umbrella & Excess Liability – Higher Risk and with Amenities

Up 25% to 100%

Workers’ Compensation

Buyers who have good to great loss histories can expect competitive rates on workers’ compensation coverage due to the profitability of carriers, contingent upon experience modification factors. As a result of the competition between carriers, these buyers can anticipate more affordable premiums.

Buyers who have good to great loss histories can anticipate more affordable premiums.

Commercial Auto

Recently, the commercial automobile sector has experienced a period of instability, wherein settlements and claim payments have had a more significant impact than profits.6 As a result, numerous carriers have been adopting telematics as a strategy to mitigate their losses.

Over the past handful of years, non-owned auto liability coverage has encountered formidable obstacles due to a persistently restricted marketplace. To address the scrutiny of underwriters in non-owned operations, certain essential elements can prove beneficial. These include driver training courses, regular vehicle maintenance, ongoing monitoring through MVR reviews, implementation of charge-back programs to incentivize improved behaviors and consideration of higher deductibles or self-insured components.

GENERAL PRICING ESTIMATES

Workers’ Compensation

Flat to Down 5%

Auto

Up 10% to 25%

Up 25% to 100%+ for Non-owned Auto Liability

Cyber

Human error accounted for 82% of data breaches in 2022, according to statistics from Nordlayer.7 Senior Housing is at a higher risk for certain types of cyber-attacks, and resources are provided and available by the U.S. Department of Health and Human Resources through the HHS Program. The most common cyber-attacks impacting this industry are: – Social engineering – Ransomware attack – Internet of Things (IoT) connected medical device vulnerabilities – Insider threats

Major Claims in The Sector

Inadequate Staffing A healthcare organization and nursing home faced a settlement of $30.9 million because of neglecting residents’ well-being and inadequate staffing at their skilled nursing facility.8 The nursing home was alleged to have engaged in harmful, negligent and deceitful behavior while caring for an elderly resident, who stayed under their supervision for around two weeks.11 Regrettably, this behavior eventually led to the passing of the elderly gentleman and caused immense anguish and distress for surviving family members.9

Data Breach Independent Living Systems, LLC experienced a data breach affecting four million individuals in their assisted living communities. HIPAA Journal noted that this was one of the largest healthcare data breaches of 2023. After notifying the individuals affected, ILS, LLC is now facing litigation by those whose information was compromised. No settlements or total cost for this incident have been reported to date.

Contact

Ryan Roberts

SVP, National Healthcare Practice Leader