Amidst a dynamic economic landscape, several significant events are shaping the business environment in the U.S. Challenges such as higher borrowing costs and inflation rates have prompted analysis of their implications for monetary policy. The Federal Reserve is closely monitoring these developments and considering adjustments to monetary policy to curb inflation while supporting economic growth. Meanwhile, shifts in employment figures and wage growth influence consumer sentiment and spending patterns as the labor market evolves. Despite challenges the reinsurance sector faces due to growing demand and losses, it remains resilient, buoyed by a favorable economic climate and increasing interest rates. Companies like Boeing are also grappling with crises which presents challenges in manufacturing flaws and labor disputes. Ongoing developments in trade relations, fiscal policy, and regulatory changes are also shaping market conditions. Understanding these critical macroeconomic trends is essential for stakeholders to make informed investment decisions and navigate market volatility effectively.

Market Outlook

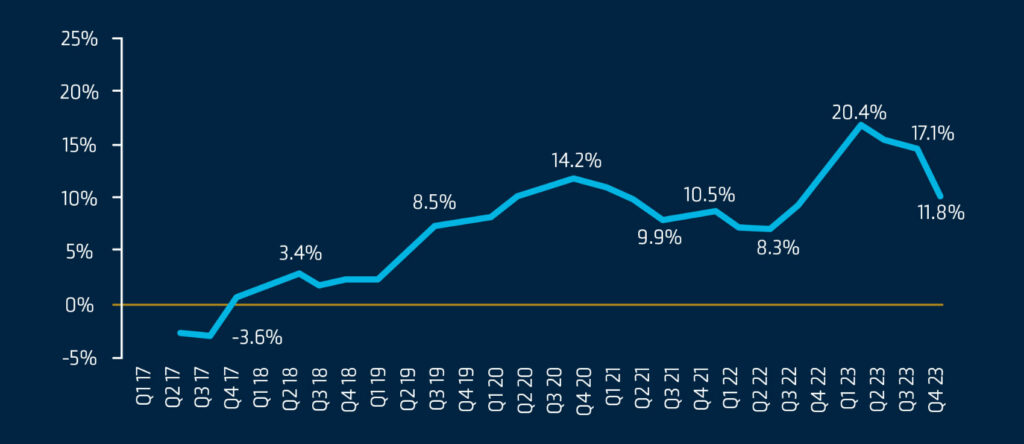

Property

Commercial property premiums increased by an average of 11.8% in Q4 2023.1

Increases to commercial property lines continue to be justified by catastrophe losses, reinsurance capacity, and pricing. Overall, these increases have been smaller or stabilized in regions such as the Midwest.

In Q4 2023, the Excess & Surplus (E&S) property market experienced a slowdown in rate increases. The slowdown is attributed to a milder hurricane season and orderly treaty renewals.2

Renewal outcomes in the market will vary based on geography, occupancy, and loss record, resulting in a diverse and segmented market.

Rising premiums and capacity constraints impact commercial property insurers, with relief anticipated for liability in 2024.3

Source: CIAB Commercial Property/ Casualty Market Index Q4 2023

General Pricing Estimates

Non-CAT-exposed property with favorable loss history

Up 11% to 19%

CAT exposed property with favorable loss history

Up 20% to 29%

Property with unfavorable loss history and a lack of demonstrated commitment to risk improvement

Up 30% to 50%+

Casualty

General Liability

Insurers are seeking additional information regarding past losses and the measures implemented to mitigate the risk of similar losses in the future.

Depending on an organization’s risk profile and loss history, commercial general liability markets will likely experience increased premiums and stricter terms and conditions.

The January 2024 premium renewal rate change for general liability lines decreased to 5.38% compared to December 2023’s 6.16%.4

Excess Liability

Carriers are pushing for rate increases in 2024 to achieve better financial results and align with loss trends.

Underwriting companies have become increasingly vocal about the escalating loss costs resulting from the ongoing deterioration in the litigation environment.5

Market cycles vary by business class, with some experiencing hardening while others softening.

Insurers navigate the challenges posed by social inflation and nuclear verdicts. The focus remains on loss ratios and monitoring reserves with lower limits to support aggregate capacity.5

Social inflation is potentially causing losses to escalate faster than general inflation by 2% to 3% annually.6

General Pricing Estimates

General Liability

Up 1% to 19%

Umbrella & Excess Liability – Middle Market

Up 1% to 19% +

Workers’ Compensation

Courts’ expansive approach to qualifying injuries for workers’ compensation coverage further increases costs.

Poor mental health impacts work safety and productivity. Businesses must prioritize mental health initiatives for a supportive workplace culture.

California, New Jersey, and New York exhibit signs of hardening due to increased claims costs from litigation and medical inflation. These states typically lead market shifts, prompting experts to monitor for potential ripple effects in 2024 and beyond.7

The long-tail nature of workers’ compensation contributes to growing financial exposure, coupled with the rising costs associated with social inflation.8

Auto

Perspectives on telematics are shifting in the insurance industry. Commercial auto insurers see telematics as a prime opportunity to steady their business and protect their bottom line against unstable loss ratios and high severity.9

In addition to concerns about weather damage and increased repair costs, there is also concern that increased vehicle thefts contribute to elevated rates. Car theft rates have increased since 2022, with Hyundai and Kia thefts making up more than half of the thefts in 2023.10

General Pricing Estimates

Workers’ Compensation

Down 1% to up 9%

Auto

Up 1% to 19% Up 20% to 30% if large fleet and/or poor loss history

Executive Risk

Directors & Officers

D&O federal securities class action claims decreased noticeably over the last three years; however, filings increased for the first time in six years, with 213 total in 2023.

The 2023 total represents an 8.1% YoY increase and is 23.1% higher than the 2010-2015 average of 173 claims per year.

Overall market conditions remain favorable in the early part of 2024. D&O pricing for recent renewals has generally been more favorable than prior years, particularly for post-IPO and post-deSPAC companies.

Many D&O carriers and reinsurers have publicly stated that current rates are unsustainable. In a December 2023 market report, reinsurer TransRe described the current D&O market as “untethered from empirical data and unhindered by logic” and, as a result, is “inadequately priced.”11

Cyber

In Q4 2023, the average cyber premium increase was under 1%.1

As emerging issues persist, there is increased caution on ransomware sub-limits, social engineering callback requirements, cybercrime exclusions on third-party funds, short restoration periods, and reputational harm-related losses.12

Threat actors are innovating new techniques to bypass security measures despite improved controls. Human error remains a significant exposure, as demonstrated in recent breaches like the MGM incident.

Underwriters are revisiting policy language to ensure stability in the face of potential large-scale cyber events.6

General Pricing Estimates

Cyber

Flat to up 10%

Major Claims In the Sector

$129 Million Verdict

The plaintiffs consumed improperly alkalinized water, forming a toxic chemical. One plaintiff underwent a liver transplant. Jurors awarded $100 million in punitive damages and over $29 million in compensatory damages.13

$44.6 Million Verdict

A plaintiff was riding a motorcycle when a delivery van struck him. At trial, evidence suggested the driver was viewing a video during the crash. Jurors awarded $44.6 million.13

Guidance

Begin the Process Early

Partner with your broker early to prepare for any changes to increase greater renewal success.

Partner with Industry Experts

It is important to work with your broker’s industry experts who understand the business and the market for placing the specific risk. Collaborating with a team that can best represent your risk and partner with your operations is more critical than ever in this disciplined market we are experiencing.

Highlight Cyber Security and Proactive Risk Management

IMA has a team solely dedicated to managing cyber risks. They offer expert assistance, including coverage analysis, financial loss exposure benchmarking, contract language review, in-depth cyber threat analysis, and strategic development of comprehensive, high- value cyber insurance programs.

Review Your Contracts

Our contract review teams add value to our clients’ overall risk management program by ensuring the indemnity language is market standard and doesn’t expose our clients to unforeseen losses that may not be insurable.

Contact

Jason Patchen

SVP, National Director of Carrier Relationships