A Few IRS Updates

IRS Letter 227

Applicable large employers across the nation are starting to become familiar with IRS Letter 226-J, which notifies the employer they may be assessed a §4980H employer shared responsibility penalty (ESRP). The current letters are focused on potential assessments for the 2015 calendar year based on the

1094-C/1095-C forms the employer reported in early 2016. Letter 226-J gives the employer just 30 days to respond and provides instructions to appeal any or all of the penalty determination. It is not a demand for payment.

IRS Letter 227 is a follow-up letter to the 226-J and is also not a demand for payment. A summary webpage indicates there are 5 versions of letter 227:

Once a final penalty determination is made, the IRS will follow up letter 227 with Notice CP220J as a Notice and Demand for Payment. Both letters 226-J and 227 provide the ability to prepay all or part of the penalty.

IRS E-Filing Threshold Changing 1/1/19

Starting January 1, 2019, the IRS intends to change the rules on when an employer is required to electronically file (e-file) the following types of tax returns:

- Form 1042-S, “Foreign Person’s U.S. Source Income Subject to Withholding”

- Forms in the 1099 series, including 1099-R issued by §401(k) or other qualified retirement plans

- Forms in the W-2 series and the corresponding W-3

- ACA information returns (1095-B, 1095-C, and the corresponding 1094)

- Several forms in the 1098 series, 5498, 8027, or other form specified by the IRS

Currently, e-filing is required when each form type results in 250 or more information returns. For example, if you issue 200 forms W-2 with a W-3 cover sheet and 100 forms 1095-C with a 1094-C cover sheet, none of them currently require the employer to e-file. And corrected information returns are

currently counted separately, resulting in rare instances where corrections must be e-filed.

Under the new proposed aggregation rules, the employer would have to aggregate the counting of all original form types combined. Using the same example, since the employers must issue 302 of these types of forms combined, then all of them must be e-filed. Also, while corrected information returns are not taken into account in determining whether the 250-return threshold is met, those meeting the 250 threshold must then e-file any follow-up correction forms for that calendar year.

IRS Grants Transitional Relief for HSA QHDHPs Complying with No-Cost Male Sterilization State Mandate

Four States and counting (Illinois, Maryland, Oregon, and Vermont) have implemented state insurance mandates requiring insured health plans issued in their State cover male sterilization as a no-cost preventive service. However, the IRS does not recognize male sterilization as preventive care, so a health savings account (HSA) qualified high deductible health plan (QHDHP) cannot pay for such services prior to the deductible being satisfied.

In an effort to provide relief for employees enrolled in employer health plans issued in any State with such a mandate, IRS Notice 2018-12 provides a transitional period for 2018 and 2019 to allow affected QHDHPs to pay for male sterilization prior to the deductible being met.

This transitional period is intended to give States time to make an adjustment to their mandates to ensure QHDHPs don’t violate federal HSA rules.

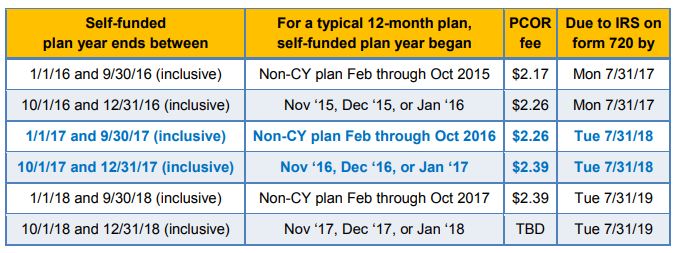

Reminder to Fil and Pay PCOR Fees by July 31

Each June we provide a reminder for employers to ensure the Patient-Centered Outcomes Research (PCOR) fee is filed and paid by July 31 on IRS Form 720.

- Insurance companies file and pay this for their insured medical plans, but employers whose insured plan is integrated with a health reimbursement arrangement (HRA) need to file and pay separately for their HRA.

- Employers with self-funded plans are responsible to file and pay on their own.

Below is a table of fees and due dates. Since the fee is based on plan year END date, we also offer an idea of when such ordinary 12-month plan years would begin, but be aware that short plan years need to be calculated based on the plan year end date (not start date) at the full rate (no pro-rating).

We are certainly happy to walk our IMA Benefits clients through more detailed instructions as needed on the counting methods, recordkeeping, etc

Please let your IMA Benefits team know if you have any questions; we will continue to monitor regulator guidance and offer meaningful, practical, timely information.