Efforts to legalize recreational cannabis continued their slow but steady progress across the U.S. in 2022 with approvals in three more states. Maryland and Missouri adopted legalization through statewide ballots, and legislation was approved and signed in Rhode Island. Currently, recreational cannabis use is legal in 21 states and the District of Columbia. Observers hold out hope that major markets like Minnesota, North Carolina and Ohio will join the mix in 2023 given that federal legalization seems further out of reach in the 118th Congress, in spite of evidence that this is a “purple” issue.

But this is just the backdrop for a bigger story as flower prices have plummeted. An extensive illicit market is one factor. Within the $72 billion U.S. cannabis industry, an estimated $47 billion takes place on the gray or black market (including cross-border sales and diverted in-state medical marijuana),1 putting licensed and tax-paying growers and retailers at a major price disadvantage.

Over-supply from in-state, licensed farms is very evident as well, due to large-scale farming and technology applications. Cannabis production in the 15 states that allow farming grew by 24% in 2022 compared to the prior year, an increase of 554 metric tons to a total of 2,834 metric tons. Oversupply was especially evident in the West. Predictably, total crop values nationwide dropped by $1 billion.2

Retail price has fallen by 75% in the past 2 years

These supply forces were magnified in Michigan. An industry-funded study found that only 30% of the cannabis sold there came through licensed channels. Much of that volume came through the state’s medical caregiver system and even more came from out-of-state – Oregon, California, and Oklahoma were identified as primary sources. Still, growers in Michigan are producing three-times more product than is sold there. The retail price has fallen by 75% in the past two years to less than $100 per ounce.3

The declining price of the flower due to these supply forces nationwide, is leading to significant financial pressure for growers in another important way. Due to Internal Revenue Code Section 280E, Cost of Goods is the only significant tax deduction available to growers, a deduction that is rapidly losing its value. Congressional efforts to address 280E will continue in 2023, but it will be an uphill fight.

Consolidation will continue to be a common survival strategy at all levels of the industry. M&A activity involving multi-state operators will continue in 2023.4 The consolidation will also be spurred by more modest industry revenue growth forecasts of 14.6% over the next five years compared to average rates that were twice that high in the previous five years.5

In this environment, growers are cutting costs wherever possible – including in their insurance coverage. Many are obtaining only the minimum coverages mandated by their states or local jurisdictions (e.g., Workers’ Compensation and, in some cases, Liability) or that are otherwise contractually required (e.g., Property). These companies are doubling down on operational risk management strategies and also self-insuring in areas like Product and General Liability through co-ops, such as CLIC Risk Retention Group, Inc., which are owned and operated by cannabis licensees at all levels of the industry.

Market Outlook

Property

Impacts have already been felt due to Hurricane Ian and other catastrophic losses throughout the year. Additionally, inflation created even more uncertainty for the difficult January 1 reinsurance renewal season.6 Property insurers experienced capacity limitations and significant rate hikes.6

With reinsurance and primary markets looking to shed some of their exposures, capacity constraints will remain the top challenge for insurance purchasers.

These capacity reductions will not only be impacting the CAT-exposed properties but also accounts with poor loss history or weak loss control protocols.

Majority of Cannabis carriers are increasing capacity to support larger facilities.

Rates are decreasing as capacity grows, underwriting will see more constraints for poor-exposed facilities, i.e., no access to water.

Overall underwriting guidelines are broadening for the cannabis industry, due to the fact that insurers are seeing positive growth and performance within their books of business.

Accounts with strong loss control, risk mitigation tactics, good loss history and proper valuations will see greater renewal success in the upcoming months.

“In instances where rates have increased, the primary driver has been reinsurance pressure.”

– CannGen Insurance

Casualty

Ending 2022, General and Excess Liability insurance purchasers experienced mostly minor price increases, as insurance companies kept trying to implement single-digit rate increases, worrying about inflation, bigger court awards and settlements.7

General Liability insurers are apprehensive about the Product Liability element of coverage for cannabis businesses, particularly those producing or marketing vaping items, edibles or drinks. A major source of concern is the potential appeal of these items to children, and the costly judgments that might stem from a lawsuit involving underage consumption.

Majority of Cannabis carriers are lowering prices in the General Liability and Product Liability lines of business, due to positive performance in trailing months.

Auto Insurers in this space are still battling an environment where many uncontrollable, outside factors are impacting business success.8 Coupled with inflation reaching a 40-year high in the U.S., auto insurers are having trouble tackling the rising frequency and severity of claims.8

Since people are driving more than they were in 2020 and 2021, there has been an increase in risky driving behaviors, which has contributed to claims outpacing rate increases.8

While auto insurers attempt to soften this line of business, alternative technology systems are being used for tracking through telematics and fleet monitoring technology.

Product Recall Traditionally, many Product Liability coverage forms only offer an “expense only” sublimit and limited coverage terms for product recalls. To address this costly coverage gap, many carriers are offering a standalone Products Recall insurance solution, which is designed to provide coverage limits for re-testing costs, loss of income, costs associated with notifying customers and other expenses connected with a product recall that would typically only be covered by the Products Liability sublimits or not at all.

One scenario where these limits might be of use is when state legislature mandates a product recall. For example, Michigan ordered a recall after identifying “inaccurate and/or unreliable results of products tested in laboratories.9”

Some carriers are expanding retroactive dates and including the purchase at inception, as an option. We can view this as insurers being responsive to the needs of the buyer.

Workers’ Compensation For the Workers’ Compensation sector, 2022 marked the eighth year in a row of successful underwriting performance.10 With the consideration of modification factors and past loss history, pricing continues to be reasonable for insurance purchasers.

Carrier competition for accounts with good to excellent loss histories will ensure that pricing will remain low.

Executive Risk

Directors & Officers (D&O) The past three years have seen a decrease in D&O litigation, an increase in dismissals and a new capacity in the marketplace, resulting in more advantageous D&O pricing for recent renewals compared to the year before.

However, despite positive pricing trends across other industries, the cannabis sector continues to be a challenge to place due to the lack of federal regulations surrounding bankruptcies in the industry.

As such and without many bankruptcies in the space to act as reference points, D&O pricing models continue to be challenged by this business.

Operators should continue to expect elevated pricing in this sector as neither of these two trends appear to be changing in the near term.

Cyber insurance is now considered a critical component

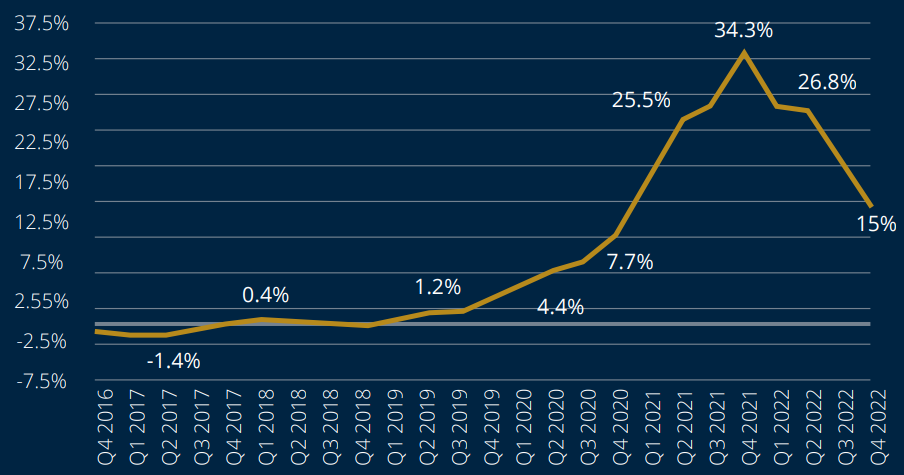

Cyber The Cyber insurance market is currently moving out of a hard market. Carriers are reallocating their portfolios in response to recent claims from 2020 and 2021, which has led to increased rates and a demand for technical controls. While ransomware claims are decreasing, the severity of other risks are still present, making this a volatile class of insurance. Despite the volatility, Cyber insurance is now considered a critical component of any organization’s risk management plan.

Pricing increases are decelerating

Increased Carrier competition over accounts

Carriers are focusing on “must have” controls and increasingly reliant on external scanning technologies in risk assessment

Specific areas of focus:

Multi-Factor Authentication (MFA)

Remote Access

Privileged users

Enterprise implementation of Endpoint Detection & Response (EDR) solution

Data backup procedures:

Detection from the network or cloud-based

Encrypted

Restricted Access

Tested

Multiple Copies

Software patch management to ensure critical security patches are made within 30 days.

Insureds that do not have satisfactory control in place may see non-renewals or reduction in coverage. This reduction comes in the form of sublimits or co-insurance provisions.

Carriers looking to reduce exposure to business interruption by reducing limits and increasing waiting periods – particularly true on contingent business interruption.

Premium Change for Cyber | Q4 2016 – Q3 2022

Source: CIAB

Major Claims in the Sector

Property Destruction Investigators reported that an illegal hemp extraction laboratory was running inside a legitimate business in an industrial park, and several explosions occurred at the location.11 It took 150 firefighters and approximately one hour to put out the flames which had rapidly reduced a one-story, 50-foot-by-100-foot building to ashes in mere minutes.11

Wrongful Death Lawsuit A Cannabis edible manufacturer was targeted in a wrongful death lawsuit filed by a family of a 28-yearold who allegedly died hours after consuming the company’s infused gummies.12 The lawsuit charged the company and several related enterprises with multiple accounts of negligence and product liability claims.12

Contaminated Marijuana Nearly 500 ounces of potentially contaminated marijuana, including some of the flower which tested positive for a fungus that can lead to lung infections or death, was quietly returned to store shelves in Michigan.13 In turn, nearly 64,000 pounds of marijuana that were deemed potentially unsafe by the state’s Marijuana Regulatory Agency (MRA) was recalled from shelves.13

Depending on the carrier, oftentimes, once the application is signed by the insured, that becomes a warranted statement. Once the risk has been underwritten, the broker presents the terms and conditions of the insurance policy and coverage is bound. It becomes a binding contract between the operator (insured) and the insurance company (insurer). Per Michael Hennessy, IMA Financial Group’s National Cannabis Practice Leader, “We encourage our clients to not think of insurance as a transaction product, but as a way to transfer risk, i.e., an insurance policy.”

Contact

Contributors

Alex Fullerton Marketing Specialist

Matt Grimes Account Executive

Michael Hennessey National Cannabis Practice Leader

Thomas, Brigette. New highs: Growing acceptance of medical and recreational marijuana will fuel industry expansion. IBISWorld Industry Report OD4141. January 2023. ↩︎

Property insurance rates to keep surging in 2023 | Business Insurance ↩︎

Liability rate hikes moderate as capacity expands | Business Insurance ↩︎

Auto insurance in 2023: 3 predictions, 3 ways to respond | PropertyCasualty360 ↩︎